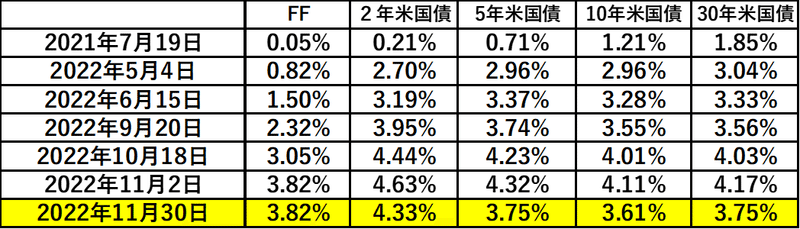

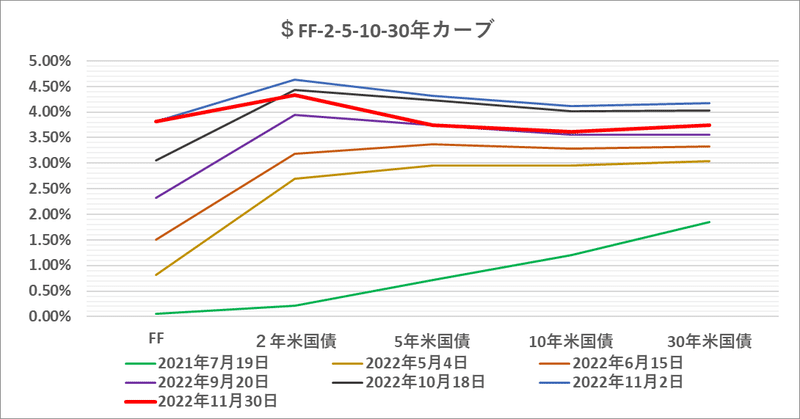

続・「米国債」と「米株価」、どっちが正しいの? - 今回のパウエル発言は "とても大事" 。

「米国債」と「米株価」、どっちが正しいの?|損切丸|note の続編。そこで挙げた2つの比較基準をここで抽出しておく:

1.「イールドスプレッド」=株価(配当利回り)と10年国債金利の比較

2.株価のキャピタルゲイン(売買差益)と金利収入の比較

さて今回のパウエル議長のスピーチだが「早ければ12月にも利上げ幅が縮小される」( ↓ 英原文)に焦点が当たっている。

” Monetary policy affects the economy and inflation with uncertain lags, and the full effects of our rapid tightening so far are yet to be felt. Thus, it makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down. The time for moderating the pace of rate increases may come as soon as the December meeting."

これを受けてNYダウ、ナスダックとも急反発したような捉え方がされているが、実はちょっと違う。今回のパウエル発言は "とても大事" なので、少し長くなって恐縮だが英原文を交えて解説したい。

今回印象的だったのが①インフレ②住宅市場③雇用について精緻なデータに基づいて論理展開されていること。正直ちょっと驚いた。

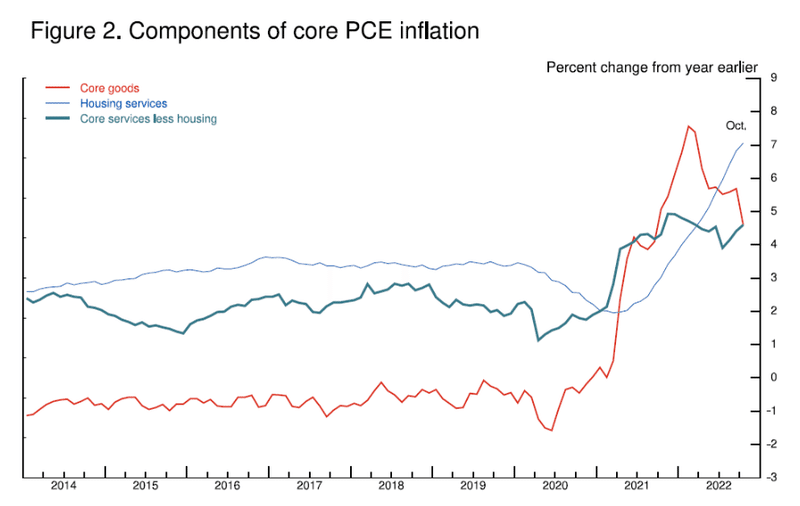

まず①インフレについては異例のパンデミックによる影響、特に供給面の制約について指摘しつつ、状況の改善を指摘。

"Early in the pandemic, goods prices began rising rapidly, as abnormally strong demand was met by pandemic-hampered supply. Reports from businesses and many indicators suggest that supply chain issues are now easing."

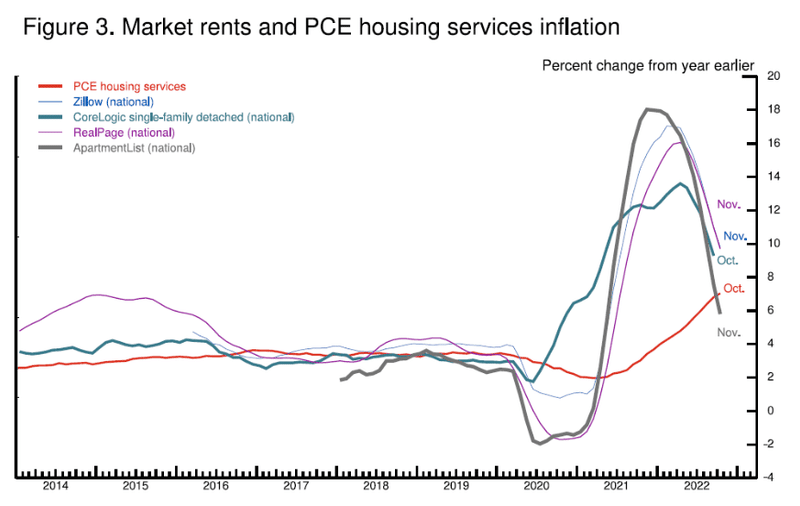

②住宅市場については一般商品の物価動向に遅れて動いており、しばらく強い数字、e.g., 過去1年で+20%、が続くものの、来年央に向けて急落すると想定。PCEの詳細 ↓ など精緻なデータを用いて分析している。

"Unlike goods inflation, housing services inflation has continued to rise and now stands at 7.1 percent over the past 12 months. Housing inflation tends to lag other prices around inflation turning points, however, because of the slow rate at which the stock of rental leases turns over. The market rate on new leases is a timelier indicator of where overall housing inflation will go over the next year or so. Measures of 12-month inflation in new leases rose to nearly 20 percent during the pandemic but have been falling sharply since about midyear."

印象的だったのはアメリカの住宅市場が構造的に供給不足にあるという点。これは常に住宅供給が居住者を上回る日本 ↓ とは全く逆。

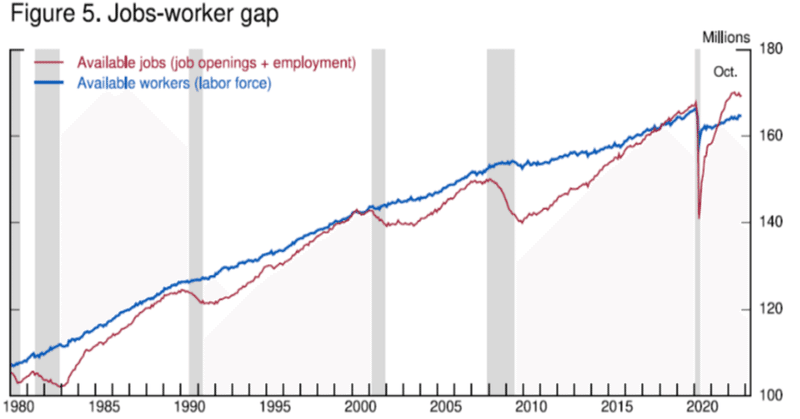

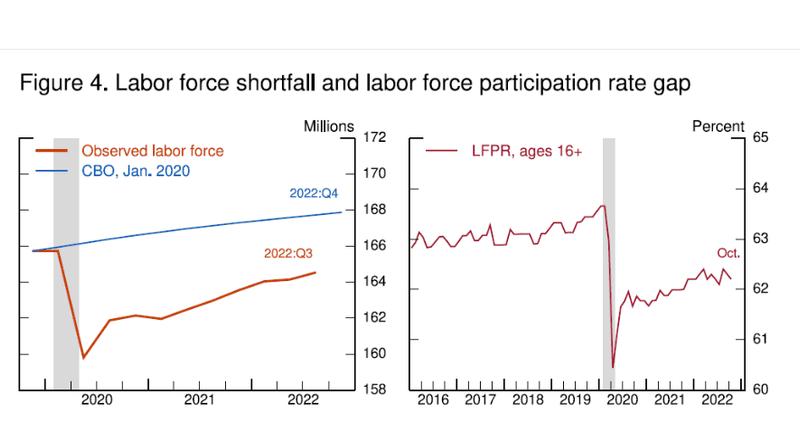

③雇用については、現在▼350万人の人手不足にあると指摘(標題グラフ ↑ )。その原因を予想を下回る人口増加と低い労働参加率にあると分析。

"Comparing the current labor force with the Congressional Budget Office's pre-pandemic forecast of labor force growth reveals a current labor force shortfall of roughly 3-1/2 million people. This shortfall reflects both lower-than-expected population growth and a lower labor force participation rate.”

400万人分の仕事が溢れていていわゆる有効求人倍率が@1.7倍に達しており、人手不足の改善は非常にゆっくりだが、過去7ヶ月で月+45万人の雇用ペースが直近3ヶ月で+29万人にまで鈍化している。

"Currently, the unemployment rate is at 3.7 percent, near 50-year lows, and job openings exceed available workers by about 4 million—that is about 1.7 job openings for every person looking for work. So far, we have seen only tentative signs of moderation of labor demand. With slower GDP growth this year, job gains have stepped down from more than 450,000 per month over the first seven months of the year to about 290,000 per month over the past three months."

FRBによる「利上げ」効果などで成長ペースは長期のトレンドを下回っており、需要が供給を上回る、いわゆる ”ボトルネック” は来年に向けて解消。住宅インフレも来年後半には目処が立つと推定。

"Growth in economic activity has slowed to well below its longer-run trend, and this needs to be sustained. Bottlenecks in goods production are easing and goods price inflation appears to be easing as well, and this, too, must continue. Housing services inflation will probably keep rising well into next year, but if inflation on new leases continues to fall, we will likely see housing services inflation begin to fall later next year."

昨日NYダウが+700ドル、ナスダックが+4%も上昇したのは「+0.75%の利上げが12月に+0.50%に縮小するから」だけではない。これだけ "説得力" のあるデータに基づいて「将来価値」に変化が生じたからだ。

今回の株価の反転は今までのように一時的な買い戻しではなく、相場の転換点になる可能性が高い。FRBが「信用」を取り戻したとも言える。

パウエル議長に対してはずっと辛口だった「損切丸」だが、これだけ精緻な分析力があるなら2021年に引締め転換も出来たはず。それだけ100年に一度のパンデミックの影響が予測困難だったのか、それとも政治の圧力で動けなかったのか。少し同情の余地があるのかもしれない(苦笑)。

1.「イールドスプレッド」で見てもS&Pはまだ@▼2%程度で "買いサイン" が出ているし、2.株価のキャピタルゲイン(売買差益)と金利収入の比較で考えても金利@4%を基準にすればNYダウは年間+1,000ドル程度は上昇するはずで、2021年終値@36,338.30まで戻っても何の不思議もない。

それもこれも現在の米国債の金利水準が「信用」に足るものなら。つまり来年央からの景気反転はFRB次第。そうすれば「米国債」「米株価」ともどちらも正しいという結末になる。

政情不安になっている日本もよくよく見てみれば、オリンピックの談合が摘発されたり実は ”正しい事” が起き始めている。「Z世代」の官僚もいるし「このままでは不味い」と思っている向きも多いのかもしれない。増税路線を続けるためにも、こういう ”間違っている事” を正すのは必須。あとは金融政策ということになるが...。中国の "暴動" も同根だろう。

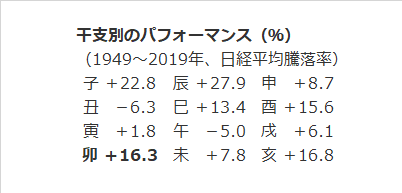

2022年は投資家受難の年だったが、こう考えていくと2023年は意外といい年になるかもしれない。過去の「干支別データ」を見ても卯年は亥(イノシシ)に次ぐ2位の@+16.3% ↓ 。そんなに悪い事ばかりは続かない。

この記事が気に入ったらサポートをしてみませんか?