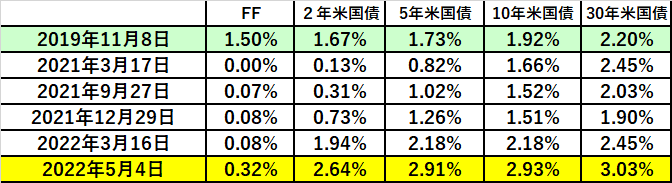

「金利」より「量」。 ー FOMC@5/4より。

”6月+0.75利上げ否定で株に買い安心感。米株価が+3%急反発”

?? 確かに ”Sell the rumour, Buy the Fact" (噂で売って事実で買え)を地で行く相場にはなったが、↑ の記事はいただけない。いかにも「経済専門記事」のようにも見え、この方が ”ヒット率” が稼げるのかもしれないが、申し訳ないが相変わらず "ずれている"(苦笑)。

今回のFOMCで重要なのは明らかに「金利」より「量」。

英語(原文まま)で量も多くて恐縮だが、QT(Quantitative Tightening、量的引締)に関して大事な記述 ↓ があったのでほとんどそのまま記載する。のちに解説は加えるが、興味のある方は目を通して頂きたい。

Plans for Reducing the Size of the Federal Reserve's Balance Sheet

Consistent with the Principles for Reducing the Size of the Federal Reserve's Balance Sheet that were issued in January 2022, all Committee participants agreed to the following plans for significantly reducing the Federal Reserve's securities holdings.

~ to reduce the Federal Reserve's securities holdings over time in a predictable manner ~ . Beginning on June 1, principal payments from securities held in the SOMA (System Open Market Account)will be reinvested to the extent that they exceed monthly caps.

For Treasury securities, the cap will initially be set at $30 billion per month and after three months will increase to $60 billion per month. ~ include Treasury coupon securities and, to the extent that coupon maturities are less than the monthly cap, Treasury bills.

For agency debt and agency mortgage-backed securities, the cap will initially be set at $17.5 billion per month and after three months will increase to $35 billion per month.

~ to maintain securities holdings in amounts needed to implement monetary policy efficiently and effectively in its ample reserves regime.

To ensure a smooth transition, ~ to slow and then stop the decline in the size of the balance sheet when reserve balances are somewhat above the level it judges to be consistent with ample reserves.

Once balance sheet runoff has ceased, reserve balances will likely continue to decline for a time, reflecting growth in other Federal Reserve liabilities, until ~ that reserve balances are at an ample level.

Thereafter, ~ will manage securities holdings as needed to maintain ample reserves over time.

「損切丸」の評価 : 随分 "QT" に ”手心” が加えられている

1. "QT" のペースを落とした

6/1から始まるが、当初3ヶ月は予定の半分=米国債▼300億ドル+MBS▼175億ドル=▼475億ドル(約▼6.1兆円)。FRBが保有する債券の償還元金+利息は除くとあるので、その分は再投資に回る。

2. "Ample Reserve" (十分な準備預金)

度々出てくるこの表現。簡単に言うと臨機応変に "QT" 操作が行われるということ。来たるべき資産価格の下落などの事態に備えるためだろう。

「株本位制」のアメリカとしてはまあ当然と言えば当然の措置。年初来時価総額が▼5兆ドル近く減少している事態に鑑みれば、株式市場に大分気を遣っているのは明らか。この声明文を受けて株価が反発したのも頷ける(まあ面倒臭くて記事にはしにくいが...)。

ただここで問題になるのが:「本当にこれでインフレを防げるのか?」

注目しなければいけないのは、株価上昇に①金利低下②原油などエネルギー価格上昇③ドルの下落を伴っている点。特に②。「株価維持」に主眼を置けば、どうしても「インフレ」抑制は緩くなる。

2021年前半の時点で6ヶ月「利上げ」が遅れた失敗を取り返すには ”手心” は不要なはず。再三再四政府サイドからの ”無茶振り” がある事には同情するが、これでは何の為に「利上げ」を急いでいるのかわからなくなる。

実際2022年「投資」では債券等「金利物」はボロボロ、株価もマイナスの中で、例えば年初来WTIが+60%も上がるなどエネルギーの一人勝ち状態。加えてこの ”手心” では「インフレ」が突っ走るのは必定。確かに株価はアメリカにとっての生命線だが、 "QT" 効果は限られる。

なので昨日(5/4)の米株価の急反発を手放しでは喜べない。逆に不安になったのは筆者だけではあるまい。まさに 常に「逆の目」はある。ー @126円超えの「円安」が起こす "変化" 。|損切丸|note 。

もっとも「インフレ税」を目論む財務当局にとっては理想的でさえあり、「税」を徴収される側は 「逆の目」を良く考えておく必要がある。最悪1970年台の「高インフレ」再現も見えており、「お金」「預金」保有者にとっては最悪の展開。そう、「預金大国」日本が最も危ない。

この記事が気に入ったらサポートをしてみませんか?