西側諸国は金価格のコントロールを失いつつある/Seeking Alphaを読む

The West Is Losing Control Over the Gold Price

西側諸国は金価格のコントロールを失いつつある

An important change has unfolded in the global gold market. The East has been driving up the gold price, predominantly in late 2022 and the first months of 2023, breaking the West’s long standing pricing power.

世界の金市場に重要な変化が起きています。 主に2022年後半から2023年最初の数か月間、東側が金価格を押し上げ、西側の長年にわたる価格決定力を打ち破った。

Until recently, Western institutional money was driving the price of gold in wholesale markets such as London, mainly based on real interest rates. Gold was bought when real rates fell and vice versa. However, from late 2022 until June 2023 gold was up 17% while real rates were more or less flat, and Western institutions were net sellers. Most likely, Eastern central banks, and Turkish and Chinese private demand, lifted the price of gold.

最近まで、西側の機関投資家マネーが、主に実質金利に基づいて、ロンドンなどの卸売市場で金の価格を動かしていました。 実質金利が下落すると金が買われ、その逆も同様です。 しかし、2022年後半から2023年6月にかけて、実質金利はほぼ横ばいながら、金は17%上昇し、西側機関投資家は売り越しとなった。 おそらく、東側の中央銀行とトルコと中国の民間需要が金の価格を押し上げたのだろう。

Introduction

導入

For about ninety years, up until 2022, there was a pattern of above-ground gold moving from West to East and back, in sync with the gold price falling and rising. Western institutions set the price of gold and bought from the East in bull markets. In bear markets the West sold to the East. For more information read my article: The West–East Ebb and Flood of Gold Revisited.

2022年までの約90年間、金価格の下落と上昇に同期して、地上の金が西から東へ移動し、また戻ってくるパターンがあった。 西側の機関が金の価格を設定し、強気市場で東側から金を購入しました。 弱気相場では西側が東側に売りました。 詳細については、私の記事「The West–East Ebb and Flood of Gold Revisited」を参照してください。

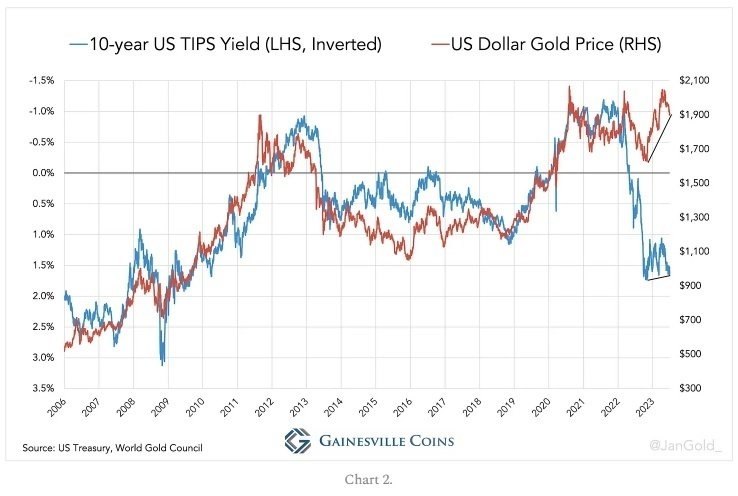

If we zoom in on the period from 2006 through 2021 the main reason for Western institutions to buy or sell gold was the 10-year TIPS rate, which reflects the 10-year expected real interest rate (“real rate,” in short) of US government bonds.

2006 年から 2021 年までの期間に注目してみると、西側機関が金を売買する主な理由は 10 年物 TIPS レートでした。これは 10 年間の米国国債予想実質金利 (略して「実質金利」) を反映しています。

The physical gold price was predominantly set in the London Bullion Market and to a lesser extent Switzerland. Gold trade in London can be divided in three categories:

金の現物価格は主にロンドンの地金市場で決定され、程度は低いですがスイスでも決定されました。 ロンドンでの金取引は 3 つのカテゴリーに分類できる。

Institutions buying and selling “large bars” (weighing 400 ounces) outrigh「大型バー」(重さ 400 オンス)を完全に売買する機関。

Trading in large bars via Exchange-Traded Funds (ETFs). 上場投資信託(ETF)を介した大型バーでの取引。

Arbitragers buying and selling in London to profit from price discrepancies between the COMEX futures price and London spot. In this sense London serves as a warehouse for the COMEX futures exchange. 裁定取引業者は、COMEX 先物価格とロンドン現物の価格差から利益を得るためにロンドンで売買する。 この意味で、ロンドンはCOMEX先物取引所の倉庫として機能する。

As we will see below, the TIPS rate, UK net gold import (positive or negative), Western ETF holdings, and the COMEX open interest were all correlated to the price of gold. Until the war in Ukraine broke out late February 2022, that is, and things started to change.

以下に示すように、TIPS レート、英国の金純輸入 (プラスまたはマイナス)、西側 ETF 保有高、および COMEX 建玉はすべて金価格と相関していた。 つまり、2022年2月下旬にウクライナ戦争が勃発し、状況が変わり始めるまでは。

Because customs data lags a few months, and the World Gold Council’s supply and demand data is published quarterly, we will cover the global market until June 2023 in this article. We will examine how gold is becoming less sensitive to real rates, and how London is losing its gold pricing power.

税関データには数か月の遅れがあり、ワールド ゴールド カウンシルの需要と供給のデータは四半期ごとに発表されるため、この記事では 2023 年 6 月までの世界市場について説明する。 私たちは、金がどのように実質金利の影響を受けにくくなっているのか、そしてロンドンがどのように金の価格決定力を失いつつあるのかを検証していく。

The West is Losing its Gold Pricing Power

西側諸国は金価格決定力を失いつつある

Let’s start by reviewing the correlation between real rates and gold. Note, the TIPS yield axes in the charts below are inverted because higher rates caused lower gold prices and vice versa.

まずは実質金利と金の相関関係を確認してみよう。 以下のチャートの TIPS 利回りの軸は、金利の上昇により金価格の下落が生じ、逆もまた同様であるため、反転されていることに注意して欲しい。

From March until September 2022 the TIPS yield rose dramatically (down in the chart), but the price of gold reacted less bearish than the “rates model” previously prescribed. As London was still a net exporter over this time horizon, I conclude the West was still in charge of the price. But then came the third quarter of 2022.

3月から2022年9月まで、TIPS利回りは劇的に上昇したが(チャートでは下降)、金価格は以前の「金利モデル」の規定よりも弱気に反応しなかった。この期間中、ロンドンは依然として純輸出国であったため、私は欧米がまだ価格の主導権を握っていたと結論づけた。しかし、2022年の第3四半期がやってきた。

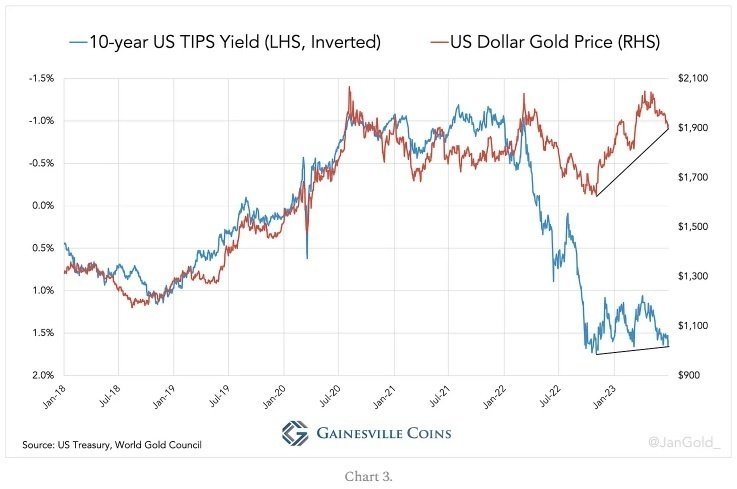

From late October 2022 until June 2023 the TIPS rate was barely down while gold was up 17%. Remarkably, the West wasn’t driving up the gold price, as demonstrated by UK net exports, declining Western ETF inventory, and falling COMEX open interest.

2022年10月下旬から2023年6月まで、TIPSレートはほとんど低下せず、金は17%上昇しました。 注目すべきことに、英国の純輸出、西側のETF在庫の減少、COMEX建玉の減少が示すように、西側諸国は金価格を押し上げていなかった。

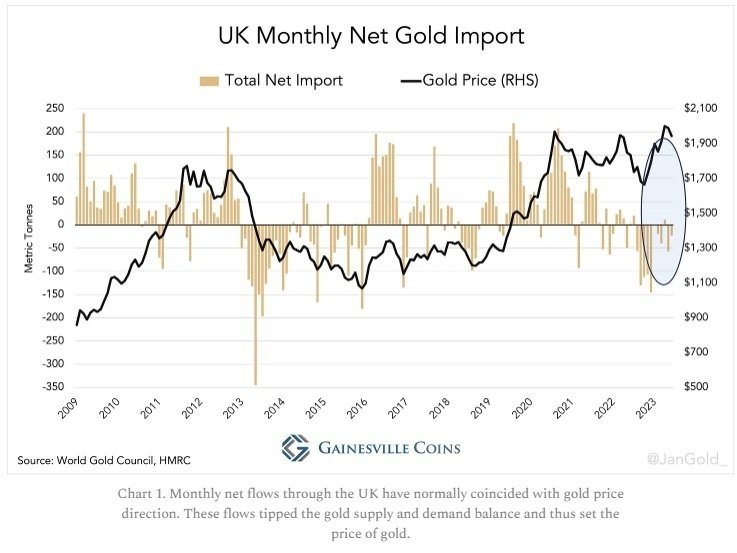

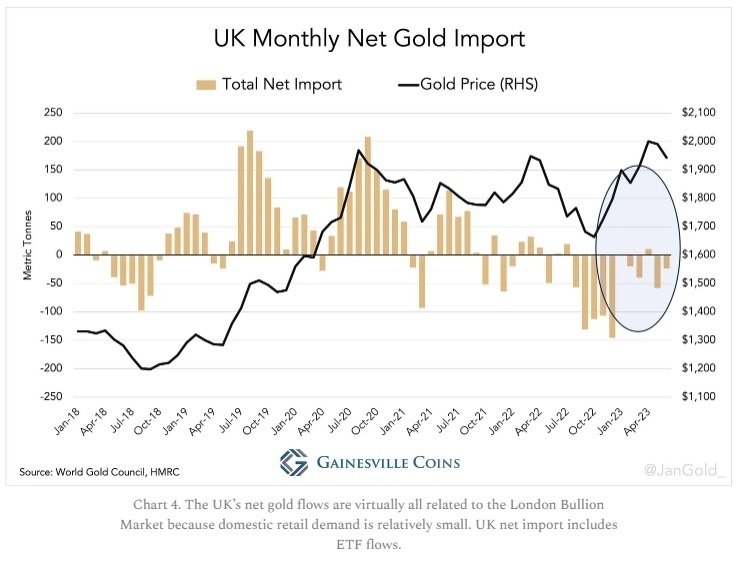

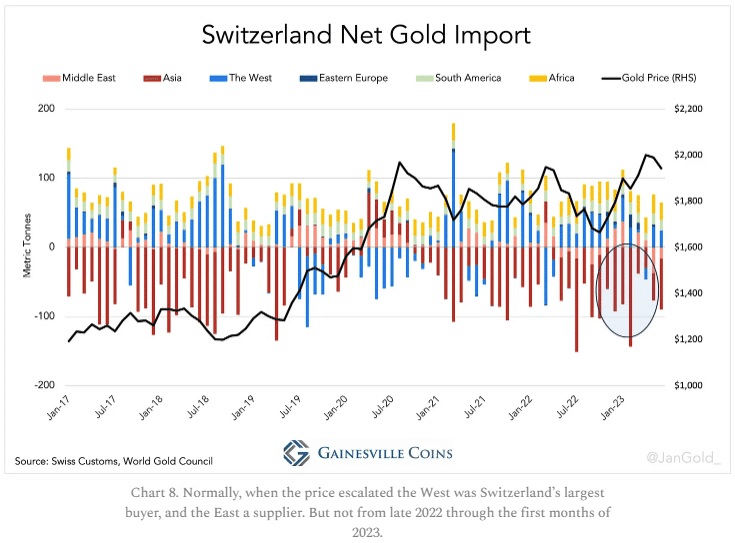

First, the UK’s monthly net flows. Obviously, the price wasn’t set in London, as the UK was a net seller while the price was up. In Chart 1 and 4 you can see this is unprecedented.

まず、英国の月間純流入額。 英国は価格が上昇している間は売り越しだったため、価格はロンドンで設定されたものではないことは明らかだ。 グラフ 1 と 4 を見ると、これが前例のないものであることがわかる。

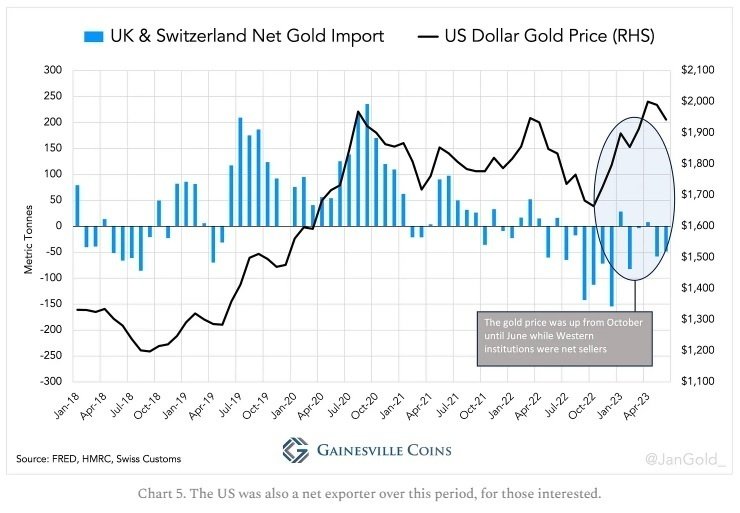

Also taking into account gold flows through Switzerland, the second largest Western physical gold market and largest refining hub globally, shows a similar picture. For the first time since monthly data is available, the gold price has been rising over several months while the UK and Switzerland combined are net exporters.

また、欧米の金現物市場第二位であり、世界最大の精錬拠点であるスイスを経由する金の流れを考慮しても、同様のことがわかる。月次データが入手可能になって以来初めて、英国とスイスが純輸出国でありながら、金価格は数ヶ月にわたって上昇している。

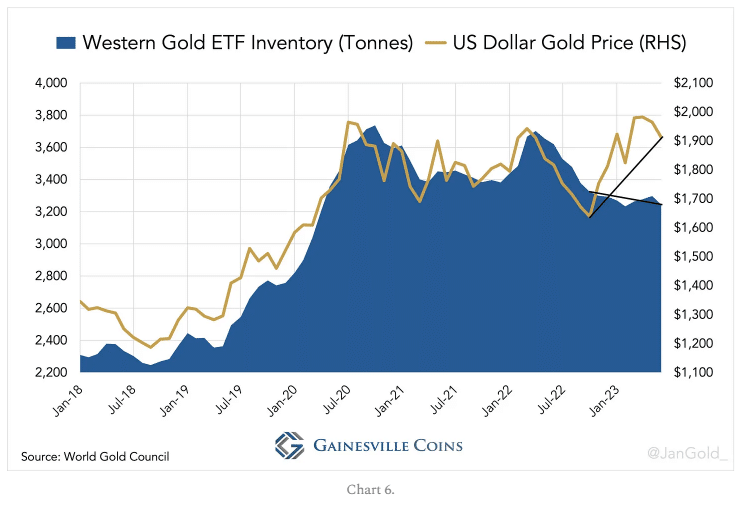

Not surprisingly, Western ETF inventory, of which the majority is stored in London and Switzerland, has declined over the past three quarters.

驚くことではないが、大部分がロンドンとスイスに保管されている欧米ETF在庫が過去3四半期で減少している。

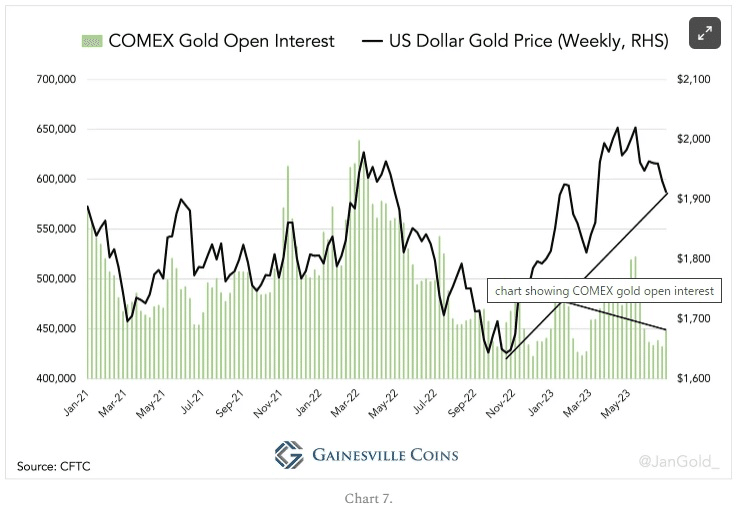

Western institutions that trade gold outright or use ETFs are dominant on the COMEX futures exchange as well. At the COMEX we see the same development: gold’s open interest has fallen over the period in question.

COMEX先物取引所でも、金の直接取引やETFを利用する欧米の金融機関が優勢である。COMEXでも同じ展開が見られる。金の建玉は問題の期間中減少している。

The East on a Gold Buying Spree

金の買い占めに沸く東側

If the UK and Switzerland were net exporters, who did they sell to? The UK mainly exported gold to Switzerland, so to answer this question all we have to do is find out which countries Switzerland exported to and check if these countries didn’t sell the metal on.

英国とスイスが純輸出国だった場合、誰に販売したのだろうか? 英国は主にスイスに金を輸出していたため、この質問に答えるには、スイスがどの国に輸出していたかを調べ、それらの国が金を販売していないかどうかを確認するだけで済む。

The Swiss customs department lets users track the flow of goods per continent. Apparently, Switzerland was a huge net exporter to Asia when the gold price went up.

スイスの税関では、大陸ごとの商品の流れを追跡することができる。金価格が上昇したとき、スイスはアジアへの巨額の純輸出国だったようだ。

Let’s see which of Switzerland’s main buyers in Asia could have pushed up the gold price.

アジアにおけるスイスの主な購入先のうち、金価格を押し上げた可能性があるのはどこなのか見てみよう。

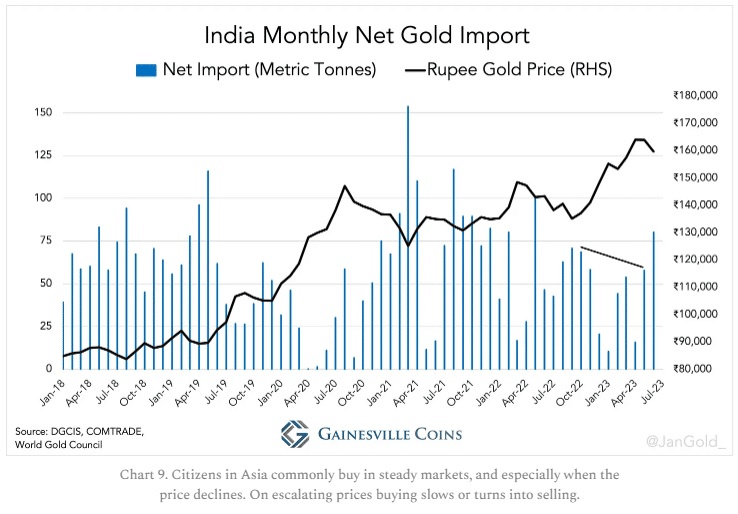

It wasn’t India, as the Indians, like most people in the East, are price sensitive. From October through June India’s net gold imports declined, with the exception of June when the price reverted.

インド人は東洋のほとんどの人々と同様、価格に敏感なので、それはインドではなかった。 10月から6月にかけて、価格が反転した6月を除き、インドの金純輸入量は減少した。

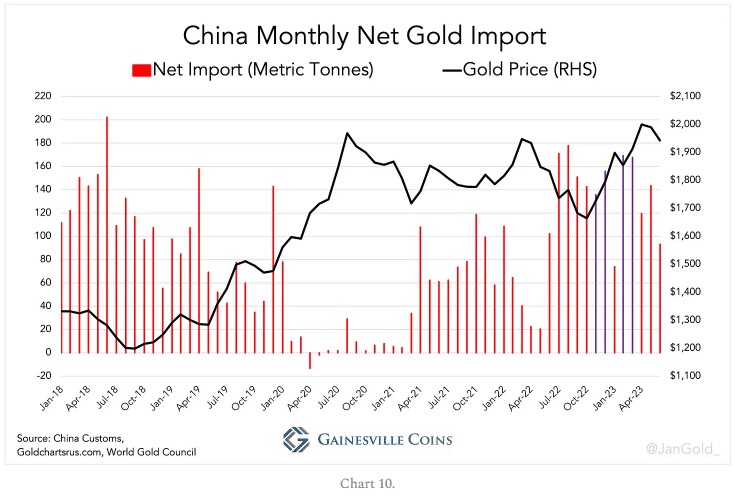

Possibly, Chinese private demand somewhat lifted the gold price. Although the Chinese are usually price sensitive, net imports into the mainland were surprisingly strong in November and December 2022, and in February and March 2023.

おそらく中国の民間需要が金価格をいくらか押し上げたのだろう。 中国人は通常価格に敏感だが、本土への純輸入は2022年11月と12月、そして2023年2月と3月に驚くほど好調だった。

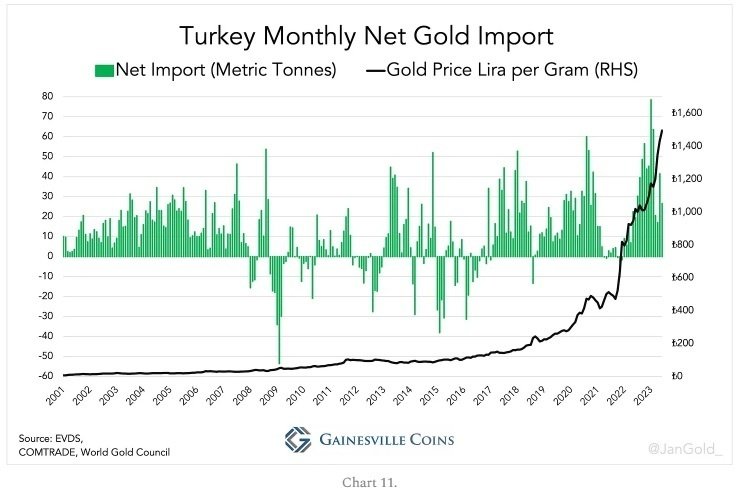

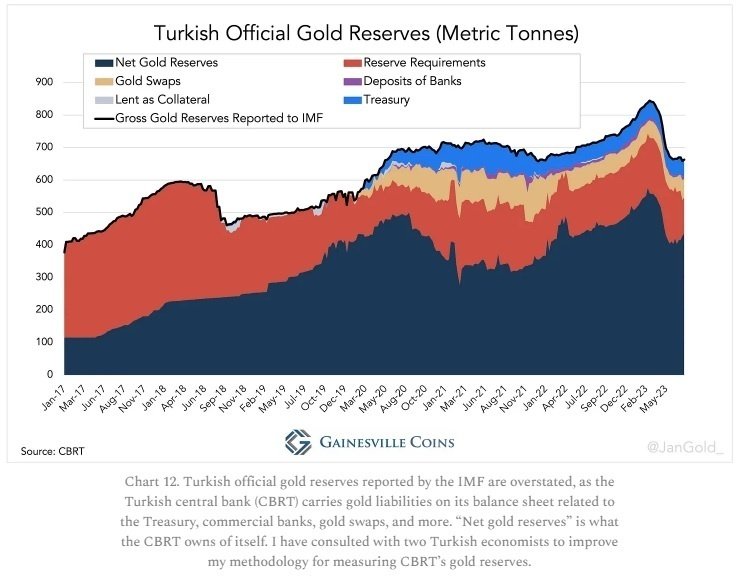

Turkey’s net import reached an all-time high in January 2023 when the Turkish lira continued to devalue and the Turks fled to real estate, durable goods and, needless to say, gold. After January the Turkish central bank began blocking imports and sold 156 tonnes of its official gold reserves domestically to defend the lira. No doubt that Turkish private demand, mainly up until January, has had an impact on the gold price.

トルコの純輸入は2023年1月に過去最高に達したが、このときトルコリラの価値は下がり続け、トルコ人は不動産、耐久財、そして言うまでもなく金に逃げた。 1月以降、トルコ中央銀行は輸入阻止を開始し、リラ防衛のため公式の金準備156トンを国内で売却した。 主に1月までのトルコの民間需要が金価格に影響を与えたことは疑いがない。

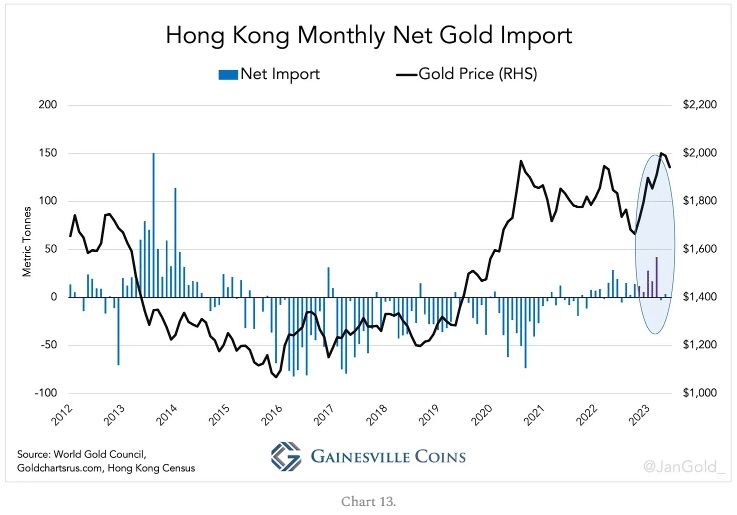

A proper indicator of a trend reversal is the net flows to Eastern trading hub Hong Kong. Normally Hong Kong would be a net importer when the price declines (and vice versa). Recently, however, Hong Kong was a net importer while the price was up. Possibly, central banks are buying in Hong Kong, monetize the gold locally, and repatriate the metal outside the scope of public customs data. Gold owned by central banks (“monetary gold”) is exempt from being reported in customs data.

トレンド反転の適切な指標は、東部貿易のハブである香港への純流入である。通常、香港は価格が下落すると純輸入国になる(逆も同様)。しかし最近、香港は価格が上昇する一方で純輸入国となっている。おそらく、中央銀行が香港で金を購入し、現地でマネタイズし、公的な税関データの範囲外で本国に送金しているのだろう。中央銀行が所有する金(「マネタリーゴールド」)は税関データでは報告されない。

The tonnages recently net imported by Hong Kong may not be very impressive, but they could be a sign of a larger development. If central banks are buying in Hong Kong they can be buying anywhere.

最近香港が純輸入したトン数はそれほど印象に残るものではないかもしれないが、より大きな発展の兆しである可能性がある。 中央銀行が香港で購入しているのであれば、どこでも購入できる。

Major suspects are non-Western central banks secretly buying gold, as dollar assets have become riskier to hold since the US seized Russia’s official dollar reserves in 2022. These central banks have an incentive not to make public rushing into gold or the price would spike excessively giving them less bang for their buck.

主要な容疑者は、2022年に米国がロシアの公式準備金を接収して以来、ドル資産を保有するのがリスクが高まっているため、非西側の中央銀行が密かに金を購入していることである。これらの中央銀行には、金への殺到を公にしないインセンティブがあり、さもなくば価格が過度に高騰することになり、 費用対効果が少なくなる。

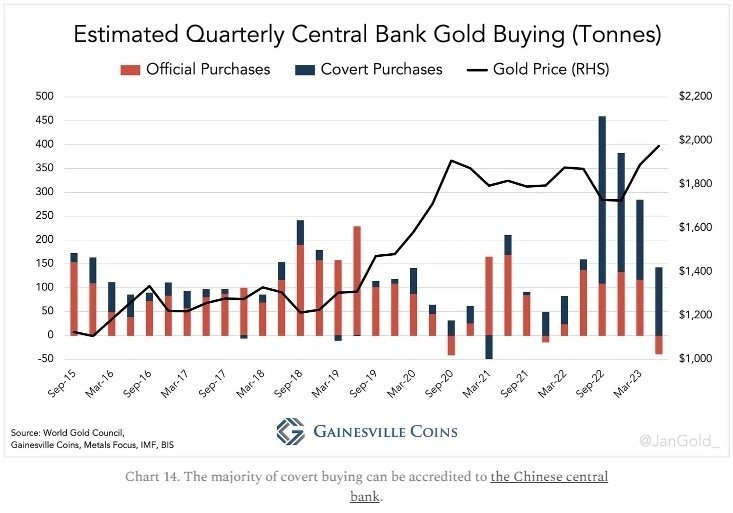

Every quarter the World Gold Council (WGC) publishes an estimate, based on field research by Metals Focus, that reflects how much they think central banks have bought. Since the Ukraine war these quarterly estimates are much higher than what central banks in aggregate report to the IMF. Most likely covert central bank purchases have boosted the price.

世界金評議会(WGC)は四半期ごとに、メタルズ・フォーカスによる現地調査に基づいて、中央銀行がどれだけの金を購入していると考えているかを反映する推定値を発表している。 ウクライナ戦争以来、これらの四半期推計値は、中央銀行がIMFに報告している総計よりもはるかに高くなっている。 中央銀行による秘密の購入が価格を押し上げた可能性が最も高い。

Conclusion

結論

The most logical explanation for gold’s recent behavior is a combination of surreptitious buying by central banks from emerging markets, and strong private demand in Turkey and China. It’s possible the WGC’s estimates of covert central bank buying are too low, given these estimates were falling during the price spike at the end of 2022 and the beginning of 2023.

最近の金の動きについて最も論理的に説明できるのは、中央銀行による新興国市場からの密かな購入と、トルコと中国の強い民間需要の組み合わせだ。 2022年末から2023年初めの価格急騰時にこの推定値が下落していたことを考えると、WGCによる秘密の中央銀行買い入れの推定値は低すぎる可能性がある。

As some of you might have noticed the US dollar gold price has been declining in the last months of the period of our investigation, and London was still a net exporter. Perhaps the West will regain control over the price again. I don’t expect the gold price to fall to levels previously suggested by the rates model though.

お気づきの方もいらっしゃるかもしれないが、調査期間の最後の数ヶ月間、米ドル建て金価格は下落しており、ロンドンは依然として純輸出国であった。おそらく、欧米は再び金価格のコントロールを取り戻すだろう。しかし、金価格が以前レートモデルが示唆したレベルまで下落するとは思わない。

Central bank buying is likely to stay strong. “We still believe that the official sector will remain a sizeable bullion buyer for the foreseeable future …, as factors that encouraged reserve managers to add gold reserves in recent years are expected to persist,” Metals Focus wrote this August.

中央銀行の買いは引き続き堅調となる可能性が高い。 メタルズ・フォーカスは今年8月、「近年、準備金管理者に金準備金の積み増しを奨励した要因は今後も続くと予想されるため、公的部門が予見可能な将来においてもかなりの規模の地金購入者であり続けると依然として信じている」と書いている。

We will have to wait and see if the East is able to further push up the price of gold and weaken the West’s control over the price. If so, gold will become less of a dollar derivative, and take more center stage in the international monetary system.

東側が金の価格をさらに押し上げ、西側による価格のコントロールを弱めることができるかどうか、見守る必要があるだろう。 そうなれば、金はドルから派生したものではなくなり、国際通貨システムの中心的な地位を占めるようになるだろう。

英語学習と世界のニュースを!

自分が関心があることを多くの人にもシェアすることで、より広く世の中を動きを知っていただきたいと思い、執筆しております。もし、よろしければ、サポートお願いします!サポートしていただいたものは、より記事の質を上げるために使わせていただきますm(__)m