第7章 線形モデル編: 第6節 Alphalensを用いて分析する

はじめに

Alphalensとは?

Alphalensとは分析に特化したpythonライブラリです。今回は本ライブラリを用いて特徴量分析を行いたいと思います。モチベーションとしましては、前回の記事で予測値を出しましたが、観測値と予測値を分析するにあたって、ICを見るだけでは物足りないので、もっと細かく分析しようという話です。

alphalensのgithubはこちらをご参照ください。

インポートと設定

import warnings

warnings.filterwarnings('ignore')from pathlib import Path

import pandas as pd

from alphalens.tears import create_summary_tear_sheet

from alphalens.utils import get_clean_factor_and_forward_returnsidx = pd.IndexSliceデータの読み込み

こちらでは前回の記事で第7章 線形モデル編: 第5節 線形回帰で株価予測をするで行った3つのモデルの出力結果を読み込みます。データセットのフォーマットとしてはscoresは残差や情報係数、アルファの情報が入っていて、predictionsが観測値と予測値である。

with pd.HDFStore('data.h5') as store:

lr_predictions = store['lr/predictions']

lasso_predictions = store['lasso/predictions']

lasso_scores = store['lasso/scores']

ridge_predictions = store['ridge/predictions']

ridge_scores = store['ridge/scores']DATA_STORE = Path('..', 'data', 'assets.h5')def get_trade_prices(tickers, start, stop):

prices = (pd.read_hdf(DATA_STORE, 'quandl/wiki/prices').swaplevel().sort_index())

prices.index.names = ['symbol', 'date']

prices = prices.loc[idx[tickers, str(start):str(stop)], 'adj_open']

return (prices

.unstack('symbol')

.sort_index()

.shift(-1)

.tz_localize('UTC'))def get_best_alpha(scores):

return scores.groupby('alpha').ic.mean().idxmax()def get_factor(predictions):

return (predictions.unstack('symbol')

.dropna(how='all')

.stack()

.tz_localize('UTC', level='date')

.sort_index()) 線形回帰

lr_factor = get_factor(lr_predictions.predicted.swaplevel())

lr_factor.head()

'''

date symbol

2014-12-09 00:00:00+00:00 AAL 0.001839

AAPL -0.001534

ABBV 0.001316

AGN 0.002175

AIG -0.000336

dtype: float64

'''tickers = lr_factor.index.get_level_values('symbol').unique()trade_prices = get_trade_prices(tickers, 2014, 2017)

trade_prices.info()

'''

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 1007 entries, 2014-01-02 00:00:00+00:00 to 2017-12-29 00:00:00+00:00

Columns: 257 entries, AAL to YUM

dtypes: float64(257)

memory usage: 2.0 MB

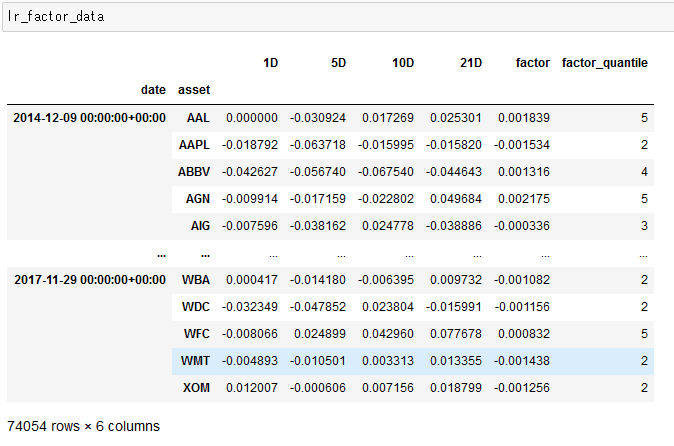

'''lr_factor_data = get_clean_factor_and_forward_returns(factor=lr_factor,

prices=trade_prices,

quantiles=5,

periods=(1, 5, 10, 21))

lr_factor_data.info()

'''

Dropped 0.0% entries from factor data: 0.0% in forward returns computation and 0.0% in binning phase (set max_loss=0 to see potentially suppressed Exceptions).

max_loss is 35.0%, not exceeded: OK!

<class 'pandas.core.frame.DataFrame'>

MultiIndex: 74054 entries, (Timestamp('2014-12-09 00:00:00+0000', tz='UTC'), 'AAL') to (Timestamp('2017-11-29 00:00:00+0000', tz='UTC'), 'XOM')

Data columns (total 6 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 1D 74054 non-null float64

1 5D 74054 non-null float64

2 10D 74054 non-null float64

3 21D 74054 non-null float64

4 factor 74054 non-null float64

5 factor_quantile 74054 non-null int64

dtypes: float64(5), int64(1)

memory usage: 3.7+ MB

'''ここでget_clean_factor_and_forward_returnsは日次データから複数のフォワードリターン(periods指定)と分位数を指定する。分位数は、ファクターをランキング付けたもので、今回は5段階評価している。最小値から最大値までを均等に5分割して、ファクターがどの階級に入っているのかを表している。これからそこも含めて詳しく分析する。

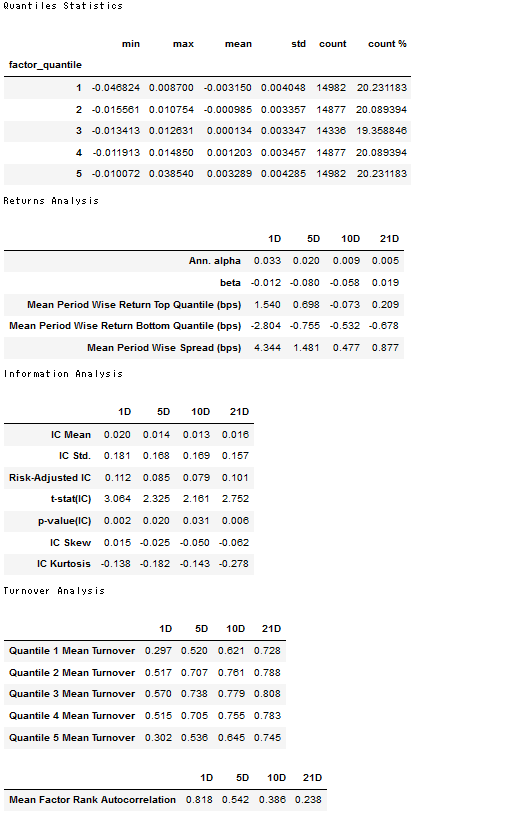

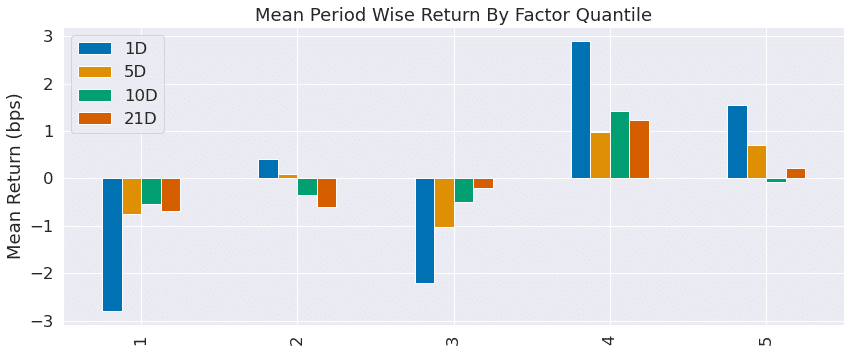

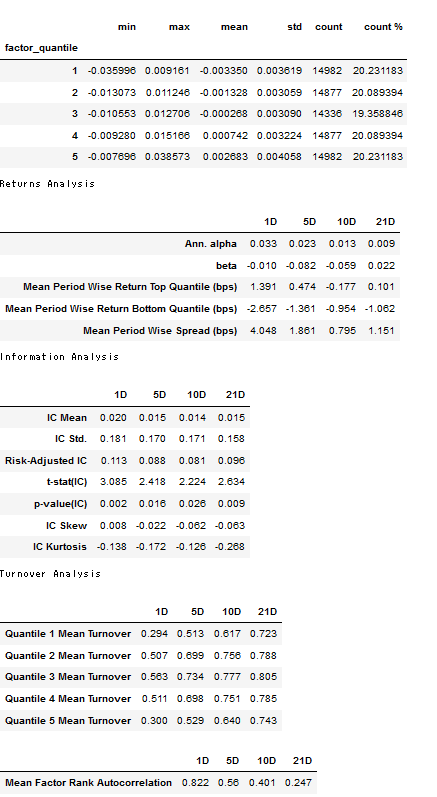

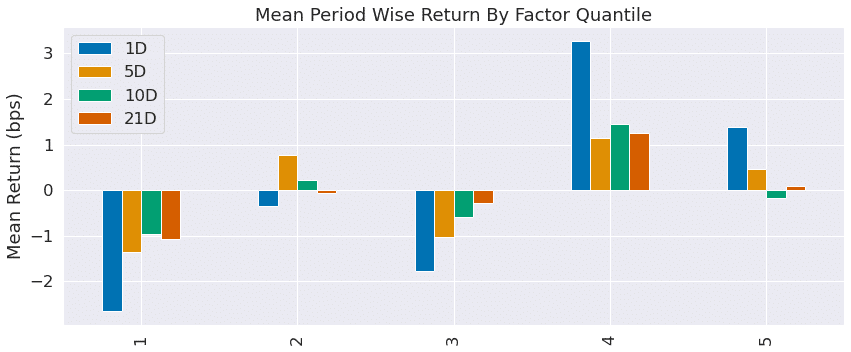

create_summary_tear_sheet(lr_factor_data);

これらの表と図がalphalens.tears.create_summary_tear_sheetで一気に呼べるんですね。残り2つの回帰に関しても同じことをやるので、解説は割愛します。

リッジ回帰

best_ridge_alpha = get_best_alpha(ridge_scores)

ridge_predictions = ridge_predictions[ridge_predictions.alpha==best_ridge_alpha].drop('alpha', axis=1)ridge_factor = get_factor(ridge_predictions.predicted.swaplevel())ridge_factor_data = get_clean_factor_and_forward_returns(factor=ridge_factor,

prices=trade_prices,

quantiles=5,

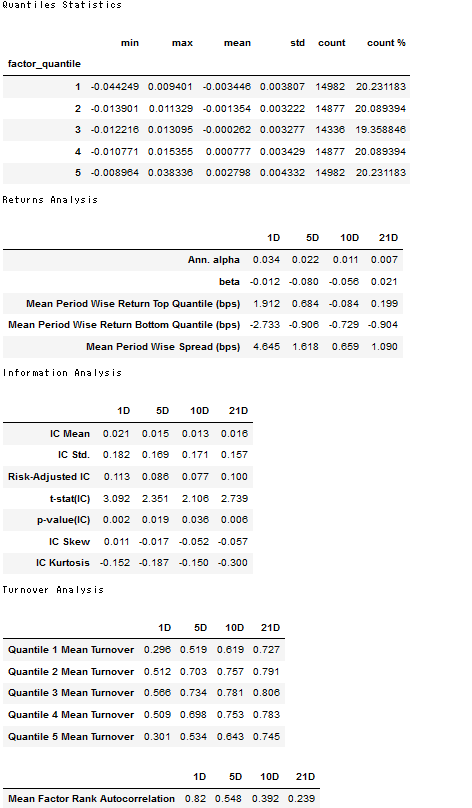

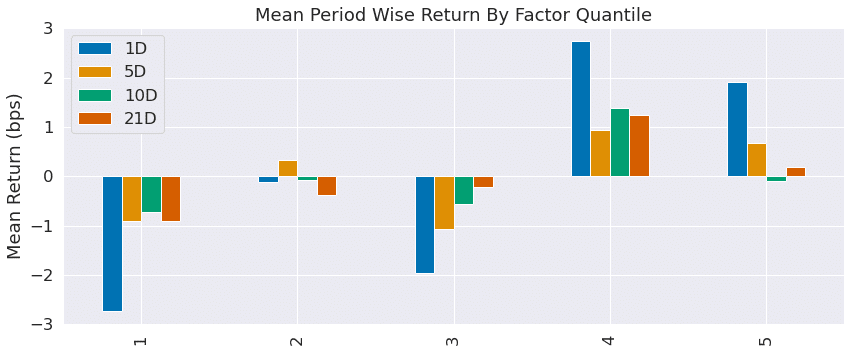

periods=(1, 5, 10, 21))create_summary_tear_sheet(ridge_factor_data);

ラッソ回帰

best_lasso_alpha = get_best_alpha(lasso_scores)

lasso_predictions = lasso_predictions[lasso_predictions.alpha==best_lasso_alpha].drop('alpha', axis=1)lasso_factor = get_factor(lasso_predictions.predicted.swaplevel())lasso_factor_data = get_clean_factor_and_forward_returns(factor=lasso_factor,

prices=trade_prices,

quantiles=5,

periods=(1, 5, 10, 21))create_summary_tear_sheet(lasso_factor_data);

この記事が気に入ったらサポートをしてみませんか?