[FAR] Lease Accounting って何?

最後の投稿からだいぶ空きましたが、Tax のシーズンがひとまず落ち着いたので投稿を再開していこうと思います。(どっかのタイミングで Schedule A - Itemized deduction- についても書いていきますのでお待ちください。)

今回の内容は Lease の Lessor と lesseeの関係、そしてどのように Journal Entry に記載していくかです。この後に Warranty の Journal Entry なんかも生地にしていく予定なのでこうご期待です笑

Lease の分類

さて、Lease Accounting においてまず重要なのは、

何年 Leaseするのか

どのように分類するのか

の2点です。

まず 1から見ていきましょう

Leaseにおいて、1年以上借りる場合、 Lessee(借りる側)はそれを capitalize することができます。つまり、Assetにカウントできるのです。それと同時に、Lease payment は liability として計上する必要はあるのですが…

ここで疑問が生じます。この lease どのように分類すればいいのかというものです。つまり、 Finance lease として I/Sに計上すべきなのか、それとも Operating lease として I/S に計上すべきなのでしょうか?

ここで2に移ります。

Finance Lease であるための条件とは !?

Finance lease か Operatig lease かの見分け方は、以下の5つのテストのうち、一つでも当てはまっているかどうかです。

つまり、Finance lease であるためには、

It is non-cancellable, and one of the five following tests met:

Transfer of Ownership Test

- Whatever you lease, transfer ownership to the lessee by the end of the leaseBargain Purchase Option Test

- Lessee has the option to purchase the lease from the owner (Lessor), and it is reasonably certain to exercise it)Lease Term Test

- The lease term is for a major part of the property's remaining economic life ---- If the lease term >= 75% economic lifePresent Value Test

- The present value of the lease payment is close to the fair value of the property. If the present value of the lease payment >= 90% of the fair value of an assetAlternative Use Test

- The asset is so specialized that it will have no value to the lessor at the end of the lease term

以上の5つのテストに一つでも当てはまったら、Finance lease として Lesseeはカウントしていきます。これは I/Sに影響があるのであって、結局 Finance であれ、Operating であれ、1年以上の leaseに関しては、 Asset と Liability への計上は変わりません。

Finance Lease 計上する方法とは?

例を使いながら解説していきたいと思います。

E.g.

Your company leases a machine for 3 years.

The machine is expected to have a residual value of $15,000 at the end of the lease. Your company will make a lease payment of $20,000 at the beginning of each year. The lessor's implicit interest rate is 6%.

さて、ここでは僕らが借りる側(Lessee)であることを思い出してください。どのように Journal Entry を考えればいいのでしょうか?

ここで注意が必要です。

問題分の数は、3年後の話をしています。つまり、3年後の Residual Value は $15,000 であっても現在の Residual Value はわかりません。

なので、Present Value (現在価値)を求めていく必要があります。

これは Lease payment も同様です。2年後、3年後に支払う $20,000の価値は当然今の $20,000の価値と違うからです。

詳しくは Time Value of Money について調べてみてください。

PV of the residual value は、3Y, 6%, FV = 15,000 で計算できます。

つまり、PV = $12,594.29 になります。

FVをプラスでPVにマイナスをつけてPVをプラスにしてもかまいません。

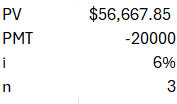

また、PV の lease payment は、Annuity Due であることも考慮し…

PV of lease payment = $56,667.85 になります。

PV of residual Value = $12,594

PV of lease payment = $56,668

Fair Value of Machine = $69,262 = $12,594 + $56,668

ようやく現在価値と、Machine の今の予想価格が出ました。

この流れを表で表すと、

になります。 (Lease Liability × 6% = Interest on Liability になります。)

Finance Lease Journal Entry

To Capitalized the Machine

The 1st Payment

The 2nd Payment

The 3rd Payment

以上が Journal Entry の流れになります。

次回は Operating Lease の時どうなるかを見ていきましょう。

お疲れさまでした。

この記事が気に入ったらサポートをしてみませんか?