経済がドイツを上回る中、イタリアの債券スプレッドは2年ぶりの低水準に低下/FTを読む

Italy’s bond spread sinks to 2-year low as economy outshines Germany

経済がドイツを上回る中、イタリアの債券スプレッドは2年ぶりの低水準に低下

Gap between the countries’ borrowing costs narrows while investors position for interest rate cuts

投資家が金利引き下げに向けて構える中、各国の借入コストの差は縮小

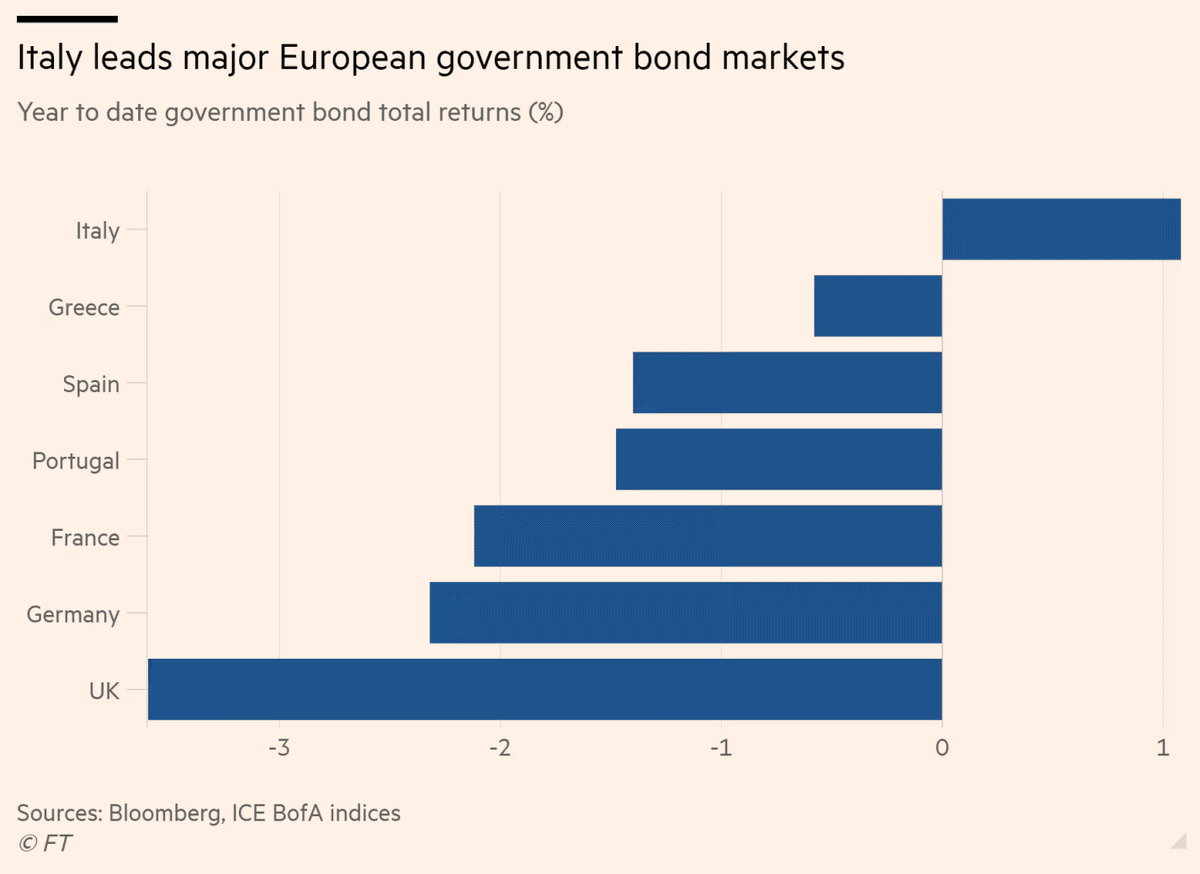

A rally in Italian government bonds has narrowed the closely watched gap between the country’s borrowing costs and Germany’s to the lowest level in more than two years, as investors become increasingly optimistic about the prospects for Italy’s economy and position for interest rate cuts.

投資家がイタリア経済の見通しと利下げの立場について楽観的になる中、イタリア国債の上昇により、注目されていた同国の借入コストとドイツの借入コストの差がここ2年以上で最低水準に縮まった。

The so-called spread, or gap, between 10-year borrowing costs in Italy and Germany sank to 1.16 percentage points on Thursday, its lowest level since November 2021, before rising back to 1.28 percentage points. That marks a major turnaround from a level of more than 2 percentage points as recently as October, reflecting growing market confidence in Prime Minister Giorgia Meloni’s handling of the economy, at a time when growth in Germany has stalled.

イタリアとドイツの10年借入コストのいわゆるスプレッド、つまり格差は木曜日に1.16%ポイントまで低下し、2021年11月以来の低水準となったが、その後1.28%ポイントに上昇した。 これは、ドイツの成長が停滞する中、ジョルジア・メローニ首相の経済対応に対する市場の信頼の高まりを反映し、10月までの2%ポイント以上の水準からの大幅な好転を示している。

“Three or four months ago, few could imagine that the spread today, in mid-March, could be 123 basis points,” Italian finance minister Giancarlo Giorgetti told the Financial Times ahead of Thursday’s moves.

イタリアのジャンカルロ・ジョルジェッティ財務相は木曜日の動きに先立ち、「3,4カ月前には、今日(3月中旬)のスプレッドが123ベーシスポイント(bp)になる可能性があるとはほとんど誰も想像できなかった」とフィナンシャル・タイムズ紙に語った。

He added that he hoped the gap in borrowing costs — known locally as “lo spread” — would “continue in this direction” to 110 basis points as Rome tried to shrink its budget deficit and easing interest rates helped lower debt servicing costs.

さらに同氏は、ローマが財政赤字の削減に努め、金利の緩和が債務返済コストの低下につながるため、地元では「ロー・スプレッド」として知られる借入コストの差が110ベーシス・ポイントまで「この方向に続く」ことを望んでいると付け加えた。

The sharp fall in the spread defies many commentators’ early fears that the election of Meloni’s rightwing bloc in September 2022 would unleash a populist spending splurge and put strain on Italy’s relationship with the EU. However, Meloni has defied those expectations, as her government has pursued a path of fiscal rectitude and forged a strong working relationship with Brussels.

このスプレッドの急激な低下は、2022年9月のメローニ氏率いる右派ブロックの選挙でポピュリストの浪費が始まり、イタリアとEUの関係に緊張が生じるのではないかという多くの評論家の当初の懸念を裏切るものとなった。 しかし、メローニ政権は財政健全化の道を追求し、ブリュッセルとの強力な協力関係を築いてきたため、メローニ首相はこうした期待を裏切った。

Concerns resurfaced last autumn when the government said it would not bring the country’s budget deficit below the limit set by the EU until 2026.

昨年秋、政府が2026年まで財政赤字をEUが設定した上限を下回らないと発表したことで懸念が再浮上した。

However, since then Italy’s economy has performed relatively well while the outlook for Germany has darkened and Chancellor Olaf Scholz’s government has lurched from crisis to crisis.

しかし、それ以来、ドイツの見通しは暗くなり、オラフ・ショルツ首相の政府は危機から危機に転落する一方で、イタリア経済は比較的好調に推移している。

The tightening of the spread also reflects investors’ hunger for high yielding assets ahead of expected European Central Bank rate cuts this summer, as well as the relative resilience of the Italian economy.

スプレッドの縮小は、今夏に予想される欧州中央銀行の利下げを控えた投資家の高利回り資産への渇望と、イタリア経済の相対的な回復力も反映している。

Benchmark German government bond yields have risen from 2.03 per cent to 2.43 per cent since the start of January, reflecting a fall in prices. The equivalent Italian borrowing costs are 3.72 per cent, slightly below the level they started the year at.

基準となるドイツ国債利回りは、価格下落を反映して1月初旬以来2.03%から2.43%に上昇している。 イタリアの同等の借り入れコストは3.72%で、年初の水準をわずかに下回っている。

The Italian public has been familiar with “lo spread” since the eurozone debt crisis more than a decade ago, when worries about Rome’s debt sustainability or a potential exit from the currency bloc caused the gap to widen dramatically to more than 5 percentage points at its peak in 2011.

イタリア国民は、10年以上前のユーロ圏債務危機以来、「ロ・スプレッド」に慣れ親しんできた。ローマの債務の持続可能性や通貨圏からの離脱の可能性に対する懸念から、2011年のピーク時には格差が5%ポイント以上に劇的に拡大した。

The falling risk premium on Italy’s debt this year is welcome news for Meloni. In recent days, she has visibly revelled in the success of recent Italian bond issues and the narrowing spreads, which she declared was a reflection of “perceptions of the solidity of the economy”.

イタリア国債の今年のリスクプレミアム低下はメローニ氏にとって歓迎すべきニュースだ。 ここ数日、同氏は最近のイタリア国債発行の成功とスプレッド縮小を目に見えて喜び、これは「経済の堅調さに対する認識」の反映だと主張した。

Italy’s economy grew in the final quarter of last year while Germany’s contracted. This unusual outperformance could continue, with the Bank of Italy forecasting 0.6 per cent growth this year, while the Bundesbank only expects 0.4 per cent for Germany.

イタリア経済は昨年の最終四半期に成長したが、ドイツ経済は縮小した。 この異例のアウトパフォーマンスは今後も続く可能性があり、イタリア銀行は今年の成長率を0.6%と予想しているが、ドイツ連邦銀行はドイツの成長率を0.4%しか予想していない。

“Italy hasn’t changed for the better or the worse, but Germany all of a sudden has become a risky country,” said Francesco Giavazzi, who served as economic adviser to former prime minister Mario Draghi. “Markets are starting to get a bit worried.”

マリオ・ドラギ元首相の経済顧問を務めたフランチェスコ・ジャヴァッツィ氏は「イタリアは良くも悪くも変わっていないが、ドイツは突然危険な国になった」と語った。 「市場は少し不安になり始めています。」

The performance of Italy’s bonds comes in spite of its huge debt pile, which rating agency Fitch forecasts will edge higher to 140.6 per cent of gross domestic product this year. In contrast, Germany’s will drop to 64.1 per cent, the agency forecasts.

イタリア国債のパフォーマンスは巨額の負債にもかかわらず生じており、格付け会社フィッチは今年の負債が国内総生産(GDP)の140.6%に達すると予想している。 対照的に、ドイツでは64.1パーセントに低下すると当局は予測している。

Italy also has a heavy issuance programme to help service its debt, with interest costs set to rise above 9 per cent of government revenues this year, the agency forecasts. Even though Italy’s budget deficit is forecast by UniCredit to shrink to 4.6 per cent this year, that is still much higher than the 2 per cent forecast for Germany.

イタリアはまた、債務返済を支援するために多額の発行プログラムを実施しており、今年の金利コストは政府歳入の9%を超える見込みであると当局は予測している。 ウニクレディトは今年のイタリアの財政赤字が4.6%に縮小すると予測しているが、それでもドイツの2%予測をはるかに上回っている。

“It’s true that Italy is doing better than Germany growth wise and that is unusual,” said Tomasz Wieladek, chief European economist at T Rowe Price. “Better macroeconomic conditions are dominating worse fiscal fundamentals.”

T・ロウ・プライスの首席欧州エコノミスト、トマシュ・ヴィエラデク氏は「イタリアがドイツより成長しているのは事実で、これは異例のことだ」と述べた。 「マクロ経済状況の改善が財政ファンダメンタルズの悪化を支配している。」

The speed of the narrowing of the spread has taken many investors by surprise. Some attribute it to appetite for higher yielding assets as the European Central Bank gets ready to begin cutting interest rates.

スプレッド縮小のスピードは多くの投資家を驚かせた。 欧州中央銀行が利下げ開始の準備を整えるなか、より高利回りの資産への需要が高まっているためだと考える人もいる。

“People have been quite taken aback over the past two weeks, the spread crossed 1.5 percentage points and since then it’s just been in freefall,” said Lyn Graham-Taylor, a senior rates strategist at Rabobank. There has been an attitude among many investors to “go long unless definitively told otherwise and enjoy the carry [higher yields]”, he said.

ラボバンクのシニア金利ストラテジスト、リン・グラハム・テイラー氏は「過去2週間で人々はかなり驚いており、スプレッドは1.5%ポイントを超え、その後はフリーフォール状態にある」と述べた。 同氏によると、多くの投資家の間には「明確に指示されない限りロングをしてキャリー(利回りの上昇)を楽しむ」という姿勢があったという。

Italian bonds have been buoyed by a flood of money from retail investors. Meloni has emphasised the importance of retail ownership of Italian debt, and the country’s ‘BTP Valore’ bonds, which are sold exclusively to individuals and provide a bonus to those who buy them at issue and hold until maturity, have raised €53.7bn since June across three tranches.

イタリア国債は、個人投資家からの資金が殺到している。メローニ首相はイタリア国債の個人保有の重要性を強調しており、個人限定で販売され、発行時に購入し満期まで保有した人にボーナスが支給される同国の「BTPヴァローレ」債は、6月以降、3つのトランシェで537億ユーロを調達している。

“It’s a very important element for us, that I am not hiding from you, that our goal is to put the greatest possible part of Italian debt in Italian hands,” said Meloni at a function on Tuesday. “The more you are the master of your debt, the more you are the master of your destiny.”

メローニ氏は火曜日の会合で「私たちにとって非常に重要な要素であるが、隠しているわけではない。私たちの目標はイタリア国債の可能な限り大部分をイタリアの手に渡すことだ」と述べた。 「あなたが自分の借金の主人であればあるほど、自分の運命の主人であることになります。」

英語学習と世界のニュースを!

自分が関心があることを多くの人にもシェアすることで、より広く世の中を動きを知っていただきたいと思い、執筆しております。もし、よろしければ、サポートお願いします!サポートしていただいたものは、より記事の質を上げるために使わせていただきますm(__)m