[FAR] Lease Accouting ②

さて、Lease Accounting の続きです。

今回は Lease Operating の時に注目していこうと思います。

お願いします。

まずは例題から

E.g.

Your company leases a machine for 3 years.

The machine is expected to have a residual value of $15,000 at the end of the lease. Your company will make a lease payment of $20,000 at the beginning of each year. The lessor's implicit interest rate is 6%.

前回と同じ例題を使ってみていきましょう。

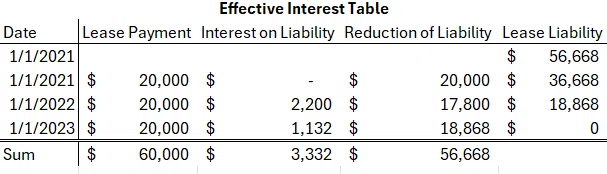

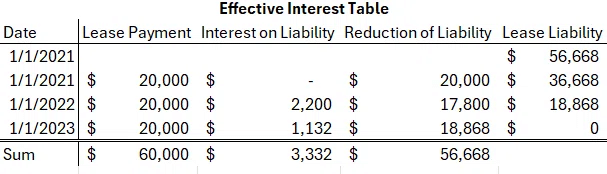

まずは前回と同様にPVを計算していきます。

PV of the residual value は、3Y, 6%, FV = 15,000 なので、

PV = $12,594.29 となります。

また、PV の lease payment は、

PV of lease payment = $56,667.85 になります。

よって

PV of residual Value = $12,594

PV of lease payment = $56,668

Fair Value of Machine = $69,262 = $12,594 + $56,668

ここまでは前回と同じです。さて、次は Journal Entry を見ていきましょう

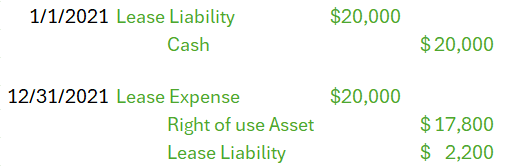

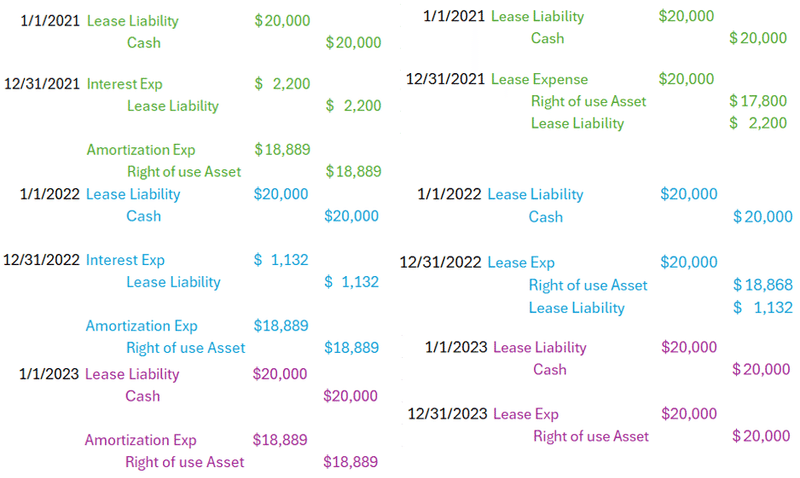

Journal Entry for Operating Lease

To capitalize on the asset

The 1st payment

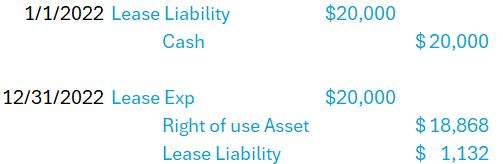

The 2nd payment

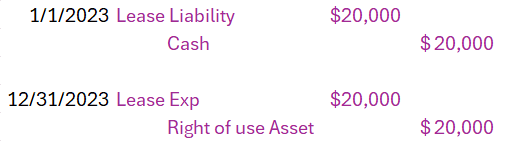

The 3rd payment

という感じになります。

ここで、Lease Lability って何?と思ったかもしれません。

これは、Lease Payable に置き換えてもらってもかまいません。

要は、Right of use Asset が Asset 計上されるので、

A = L + E の式を成立させるために作った新しい Account です。

Right of use Asset 56,668 の価値あるから

Lease Liability 56,668 使用する分をいったん計上しておこうっていうことです。

まとめ - Finance Lease と Operating Lease の違い

Finance Lease -

Separately Recognize Interest Expense and Amortization Expense

Operating Lease -

Recognize only lease expenses ( This includes interest and amortization )

結局 Finance 側の Debit の合計と Operating 側の Debit の合計に違いは出ません。 (2200 + 18889) + (1132 + 18889) + (18889) = 20000 *3 と代々同値になります。

つまり、 Lease exp と Operating では書かれていますが、それは Interest exp と Amortization Exp を包括しているのです。

今回は以上です。お疲れさまでした。

この記事が気に入ったらサポートをしてみませんか?