バブルのようなバリュエーションが2024年のナスダック100のハードルとなる/ゼロヘッジを読む

Bubble-Like Valuations Pose Hurdle For Nasdaq 100 In 2024

バブルのようなバリュエーションが2024年のナスダック100のハードルとなる

The Nasdaq 100 basket has surged an eye-popping 53% so far this year, with the gains having accelerated since the start of November thanks to markets front-running the idea policy loosening from the Fed.

ナスダック100バスケットは今年これまでに53%も目を見張るような急騰を見せており、FRBの政策緩和を先取りした市場のおかげで11月初めから上昇が加速している。

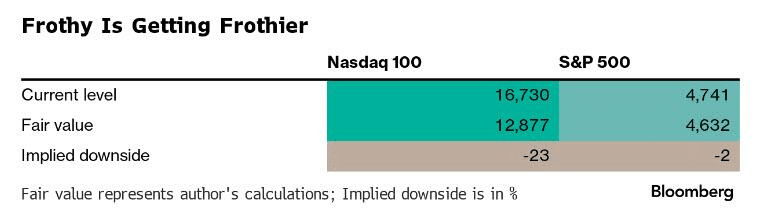

Looked at as a long-duration bond, the fair value of Nasdaq 100 is 12,877, with the assumptions underpinning the analysis laid out below.

長期債券として見ると、ナスダック 100 の公正価値は 12,877 ドルであり、分析の基礎となる仮定は以下に示されています。

As Keynes famously remarked, markets can remain irrational longer than one can remain solvent, so it’s difficult to call for a correction, but there does come a point in any bull run where valuations become so stretched as to resemble a veritable card castle.

ケインズの名言にあるように、市場は支払能力を維持できる期間よりも長く不合理な状態を維持することができるため、調整を求めるのは難しいが、どのような強気相場でも、バリュエーションが引き伸ばされ、まさにトランプの城のようになる時が来る。

[ZH: Nasdaq looks rich on a Price-to-Sales basis too...]

[ZH:ナスダックは株価対売上高でもリッチに見えるが...。]

Ironically, not all rallies are made equal, and nowhere is this more evident than with the S&P 500 that has run up more than 23% this year. Despite those gains, at the current level of 4,740, the basket is trading just 2.3% above its fair value of 4,632.

皮肉なことに、すべての上昇が同じとは限らず、今年23%以上上昇したS&P500ほどそれが顕著なものはない。このような上昇にもかかわらず、現在の水準4,740では、バスケットは公正価値4,632をわずか2.3%上回って取引されているに過ぎない。

So why is 12,877 fair value?

では、なぜ12,877ドルが公正価値なのか?

Because as Ven Ram explains, that's what one gets when looking at the technology basket is viewed as a long-duration bond.

ヴェン・ラムが説明するように、テクノロジー・バスケットを長期の債券と見なしたときに得られるものだからだ。

The analysis essentially assumes that dividends that accrue from the index will increase at a compounded annual rate of 11.4%, mimicking the growth rate over the past 10 years.

この分析では、基本的にインデックスから発生する配当が年複利11.4%で増加すると仮定しており、過去10年間の成長率を模倣するものとなっている。

It uses a discount rate of 5% and assumes that the growth rate will slow to 5% beyond a forecast horizon of 30 years

割引率5%を使用し、予測期間30年以降は成長率が5%に鈍化すると仮定している。

Using a similar analysis, the fair value of the S&P 500 is 4,632, suggesting that brick-and-mortar stocks may be reflecting saner valuations.

同様の分析によれば、S&P500のフェアバリューは4,632となり、実店舗型企業の株価がより健全なバリュエーションを反映している可能性を示唆している。

[ZH: But the S&P still looks very rich on a Price-to-Sales basis...]

[ZH:しかし、S&Pはまだ株価対売上高で見ると非常にリッチに見えるが...。]

Even so, any further upside in the basket is less than 3% from last week’s closing level.

それでも、バスケットのさらなる上昇幅は先週の終値から3%未満である。

All told, valuations in technology stocks look stretched. While some enthusiasm toward stocks related to artificial intelligence may be condoned, glaring overvaluations tilt the market toward a correction sooner rather than later.

総じて、テクノロジー株のバリュエーションは割高に見える。人工知能関連銘柄への熱狂は容認されるかもしれないが、目に余る割高感は早晩、市場を調整へと傾けるだろう。

英語学習と世界のニュースを!

自分が関心があることを多くの人にもシェアすることで、より広く世の中を動きを知っていただきたいと思い、執筆しております。もし、よろしければ、サポートお願いします!サポートしていただいたものは、より記事の質を上げるために使わせていただきますm(__)m