ライバルと投資家を驚かせる日本の半導体取引/FTを読む

The Japanese semiconductor deal spooking rivals and investors

ライバルと投資家を驚かせる日本の半導体取引

Tokyo’s $6.4bn swoop for JSR has rekindled memories of heavy state intervention and cast doubt on corporate reforms

東京によるJSRへの64億ドルの急襲は国家による激しい介入の記憶を再燃させ、企業改革に疑問を投げかけた

In June 2023, an obscure semiconductor materials supplier announced that it was set to be taken over by an investment fund in a $6.4bn deal.

2023年6月、無名の半導体材料サプライヤーが投資ファンドに64億ドルの取引で買収される予定であると発表した。

Even many Japanese have not heard of JSR, a company that embodies one of the few areas of the semiconductor industry where Japan retains dominance. It is a leading provider of so-called photoresists — specialist chemicals used for printing circuit designs on chip wafers — to chipmakers such as Samsung Electronics, Taiwan Semiconductor Manufacturing Company and Intel.

多くの日本人ですら、JSR という会社のことを聞いたことはない。JSR は、日本が主導権を保っている半導体業界の数少ない分野の 1 つを体現する企業である。 同社は、サムスン電子、台湾積体電路製造会社、インテルなどのチップメーカーに、いわゆるフォトレジスト(チップウェーハ上に回路設計を印刷するために使用される特殊化学薬品)を提供する大手プロバイダーである。

But it was the identity of the acquirer that really raised eyebrows. Japan Investment Corporation is a government-backed fund whose investments are overseen by the Ministry of Economy, Trade and Industry (Meti) — the same interventionist branch of government that dictated and crafted Japan’s industrial policy during its stunning postwar economic recovery.

しかし、本当に眉をひそめたのは買収者の正体だった。 日本投資法人は、政府支援のファンドであり、その投資は経済産業省(Meti)によって監督されている。経済産業省は、戦後の驚異的な経済回復中に日本の産業政策を決定し、策定したのと同じ介入主義的な政府部門だ。

Yasutoshi Nishimura, the head of the ministry at the time of the deal, championed it as “an extremely important effort . . . that will strengthen Japan’s global competitiveness in semiconductor materials pivotal to the production and development of cutting-edge chips”.

合意当時の同省長官の西村康稔氏は、これを「非常に重要な取り組み. . .それは、最先端チップの生産と開発に極めて重要な半導体材料における日本の国際競争力を強化するでしょう。」であると擁護した。

The transaction and Nishimura’s comments rang alarm bells among JSR’s biggest customers and investors as they tried to gauge whether government intervention would now become the norm. They soon got an answer: in December, JIC led a consortium to buy out Fujitsu’s chip-packaging arm Shinko Electric Industries for around $4.7bn.

この取引と西村氏のコメントは、政府介入が常態化するかどうかを見極めようとするJSRの大口顧客や投資家の間で警鐘を鳴らした。 彼らはすぐに答えを得た。12月にJICはコンソーシアムを主導し、富士通のチップパッケージ部門である新光電気工業を約47億ドルで買収した。

JIC’s chief executive Keisuke Yokoo recently warned that Japan’s medium-sized companies would not be able to compete against bigger global rivals on technology alone.

JICの横尾敬介最高経営責任者(CEO)は最近、日本の中堅企業は技術だけでは世界のより大きなライバルと競争することはできないと警告した。

“My thinking is that [JSR and Shinko Electric] cannot win the competition unless they continue investing in the digital era, so we want to support that effort,” he added.

「私の考えでは、(JSRと新光電気は)デジタル時代への投資を継続しなければ競争に勝つことはできない。そのため、我々はその取り組みを支援したい」と付け加えた。

The manner in which the JSR/JIC agreement was reached also rankled with many. The Financial Times revealed in January that JSR’s American chief executive, Eric Johnson, and the rest of the board had previously rejected an approach from the German group Merck that could have led to a takeover.

JSRとJICの合意に達した経緯にも多くの人が困惑した。 フィナンシャル・タイムズは1月、JSRの米国人最高経営責任者エリック・ジョンソン氏と残りの取締役会が、買収につながる可能性のあるドイツのメルクグループからのアプローチを以前に拒否していたことを明らかにした。

The existence of a serious approach, combined with the abruptness of a rare take-private offer by a government-backed fund, has caused some JSR investors to question the notion that corporate Japan was on a journey to better governance and more transparency.

政府支援ファンドによる異例の非公開化提案の唐突さと相まって、真剣なアプローチの存在により、一部のJSR投資家は、日本企業がガバナンスの向上と透明性の向上に向けて歩みを進めているという考えに疑問を抱くようになった。

That faith had helped drive the strong rally in Japanese equities. In 2023, the Nikkei 225 was one of the world’s best-performing major stock indices. It also prompted activist investors to take greater interest in Japanese companies; San Francisco-based ValueAct is a shareholder in JSR and its co-chief executive, Robert Hale, is on the company’s board.

その信念が日本株の力強い上昇を後押しした。 2023 年、日経 225 は世界で最もパフォーマンスの高い主要株価指数の 1 つとなった。 また、物言う投資家が日本企業に一層の関心を持つようになっている。 サンフランシスコを拠点とする ValueAct は JSR の株主であり、共同最高経営責任者である Robert Hale が同社の取締役会のメンバーである。

JSR and the fund bristle at any suggestion that this deal was a de facto nationalisation of a private company. A senior Meti official says the evaluation of competing bids was a matter for JSR’s board and that the government did not interfere in the affairs of private companies. The official adds that Meti would “use export controls rather than owning certain companies” to protect Japan’s national economic interests.

JSRと基金は、この取引が民間企業の事実上の国有化であるという示唆に対して激しく反発した。 経産省の高官は、競合入札の評価はJSR取締役会の問題であり、政府は民間企業の問題には干渉していないと述べた。 同当局者は、日本の国家経済利益を守るために経産省は「特定の企業を所有するのではなく、輸出規制を利用する」だろうと付け加えた。

But to JSR’s investors and customers, that is exactly what it was. “The deal, as it stood, was baffling in the context of the direction we thought the Japanese market was heading,” says one US-based fund manager who had held JSR stock for some years.

しかし、JSR の投資家や顧客にとっては、それがまさにそうだった。 「現状では、日本市場が向かうと我々が考えていた方向性を考えると、この取引は不可解だった」と、数年間JSR株を保有していた米国拠点のファンドマネージャーは語る。

“Nothing seemed to add up.”

「何も意味がないようでした。」

JSR says that it originally approached JIC in November 2022. Johnson argued that backing from the investment group, whose mission is to “enhance international competitiveness of businesses”, would help to accelerate consolidation within Japan’s chip materials industry.

JSRは、最初にJICに打診したのは2022年11月だったとしている。ジョンソン氏は、「企業の国際競争力の強化」を使命とする投資グループからの支援が日本のチップ材料産業内の統合を加速させるのに役立つと主張した。

At a time when the semiconductor industry finds itself at the centre of geopolitical tension between the US and China, “we had to do a lot of discussions with customers to make sure they understood this is absolutely not a political agenda,” Johnson told the Financial Times last year.

半導体業界が米国と中国の間の地政学的な緊張の中心にある中、「これは絶対に政治的議題ではないことを顧客に理解してもらうために、顧客と多くの議論を行う必要があった」とジョンソン氏は昨年フィナンシャルタイムス紙に語った。

“This is an economic agenda,” Johnson added. “We are getting privatised to advance economic goals for us and also for the Japanese economy.”

「これは経済的課題だ」とジョンソン氏は付け加えた。 「私たちと日本経済の経済目標を前進させるために、私たちは民営化されています。」

Few within the industry were convinced. In the weeks after the deal was revealed, Samsung, TSMC and JSR’s other big customers sought an explanation for why a listed company that was not financially struggling was hurriedly being taken private by a state-backed fund.

業界内でも納得した人はほとんどいなかった。 この取引が明らかになってから数週間で、サムスン、TSMC、JSRの他の大口顧客は、財務的に苦境に陥っていない上場企業がなぜ国の支援を受けたファンドによって急いで非公開化されるのか説明を求めた。

Their sensitivity was increased by Japan’s aspiration to compete against them via Rapidus, a company created in 2022 and backed by the government and the country’s biggest corporations. Rapidus aims to develop advanced chips with IBM that will power the next generation of smartphones, data centres and artificial intelligence.

彼らの感受性は、2022年に設立され、政府と国内最大手の企業の支援を受けている会社であるRapidusを通じて競争したいという日本の願望によってさらに高まった。 Rapidus は、次世代のスマートフォン、データセンター、人工知能を強化する高度なチップを IBM と開発することを目指しています。

Despite strong denials from the company and government advisers, JSR’s customers feared that having JIC on the board of one of their most important suppliers would give the Japanese government access to commercially sensitive information about their technology.

同社および政府顧問が強く否定したにもかかわらず、JSR の顧客は、JIC が自社の最も重要なサプライヤーの 1 社の取締役会に加わることで、日本政府が自社の技術に関する商業上の機密情報にアクセスできるようになるのではないかと懸念していた。

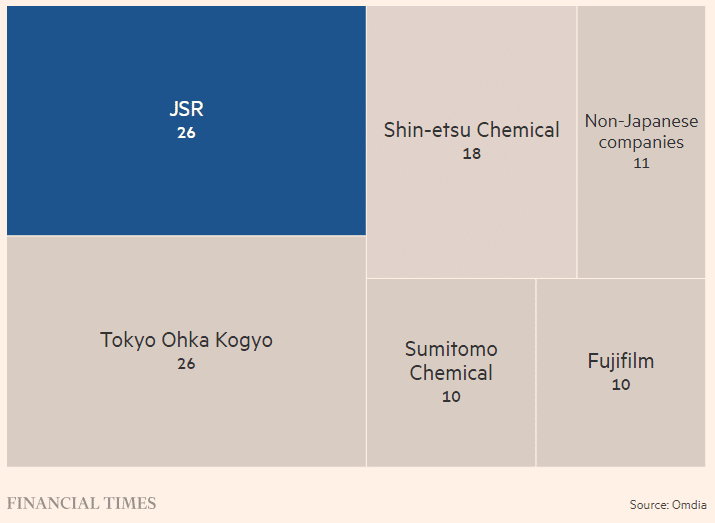

JSR’s leading position in the global photoresist market

世界のフォトレジスト市場におけるJSRのリーダー的地位

Market share by company (%, 2021)

企業別市場シェア (%、2021 年)

That led some executives close to JSR to worry that rather than increasing its share of the global photoresists market, the transaction could potentially drive customers away.

このため、JSRに近い一部の幹部は、この取引により世界のフォトレジスト市場でのシェアが拡大するどころか、潜在的に顧客を遠ざける可能性があると懸念した。

“The damage has already been done,” one of the executives says, although others close to JSR’s largest customers say the company’s executives have addressed their initial concerns about the JIC investment and that they expect to continue sourcing from JSR.

幹部の1人は「被害はすでに出ている」と語るが、JSRの最大顧客に近い関係者らは、同社幹部はJIC投資に対する当初の懸念に対処しており、JSRからの調達を継続する予定だと述べている。

JIC said the government would not be involved in the affairs of an individual company and that there was a need to explain to JSR’s customers that such concerns were “unfounded”.

JICは、政府は個別企業の問題には関与しないとし、そのような懸念は「根拠がない」ことをJSRの顧客に説明する必要があると述べた。

TSMC said it “maintains a strong and close partnership with its suppliers, which includes open communication channels and strict co-operation on technology confidentiality management”. Samsung declined to comment. A person close to JSR said its customer ties were “strong as ever” after explaining the strategic rationale for the JIC deal.

TSMCは「サプライヤーとの強力かつ緊密なパートナーシップを維持しており、これにはオープンなコミュニケーションチャネルや技術機密管理における厳格な協力が含まれる」と述べた。 サムスンはコメントを控えた。 JSRに近い関係者は、JICとの取引の戦略的根拠を説明した後、顧客との絆は「相変わらず強い」と述べた。

Concerns were also raised by Chinese customers. The launch of the tender offer through which JIC will acquire JSR’s listed shares has been pushed from late December to at least late February because of delays with a Chinese antitrust review.

中国人顧客からも懸念の声が上がった。 JICがJSRの上場株式を取得する公開買い付けの開始は、中国の独禁法審査の遅れにより、12月下旬から少なくとも2月下旬に延期された。

“The possibility now seems to be rising that Chinese authorities will not approve the transaction and the deal will not materialise,” says Kazuyoshi Saito, an analyst at IwaiCosmo Securities. Reflecting the uncertainty, JSR shares currently trade around ¥4,000, below the ¥4,350 offered by JIC.

岩井コスモ証券のアナリスト、斉藤和義氏は「中国当局が取引を承認せず、合意が実現しない可能性が高まっているようだ」と話す。 不確実性を反映して、JSR株は現在4,000円付近で取引されており、JICが提示した4,350円を下回っている。

Rival materials suppliers have also dismissed the idea that government backing for JSR will help to restructure the industry. The company’s previous attempts to merge its chips materials business with competitors failed, and so far there is little indication that the landscape has changed, they say.

ライバルの材料サプライヤーも、JSRに対する政府の支援が業界の再編に役立つという考えを否定している。 チップ材料事業を競合他社と統合するという同社の以前の試みは失敗に終わり、今のところ状況が変わった兆候はほとんどない、と彼らは言う。

Noriaki Taneichi, chief executive of Tokyo Ohka Kogyo, another Japanese chips materials maker, has openly questioned how the deal would benefit JSR’s customers. “I have considered it from various angles but this deal doesn’t make sense,” Taneichi said at an earnings briefing in August.

同じく日本のチップ材料メーカーである東京応化工業の種市順明最高経営責任者(CEO)は、この取引がJSRの顧客にどのような利益をもたらすのかについて公然と疑問を呈している。 種市氏は8月の決算説明会で「さまざまな角度から検討したが、今回の合意は意味がない」と述べた。

“If they are talking about consolidation within the photoresist industry, I hope it ends up going nowhere.”

「彼らがフォトレジスト業界内での統合について話しているのであれば、それが無駄に終わることを願っています。」

For investors, the conduct of the acquisition process was a cause for concern. Interviews with current and former executives of JSR, government officials, investors, bankers, private equity firms and industrial rivals with direct knowledge of the deal show that the saga did not start with JSR’s overtures to JIC in November 2022.

投資家にとって、買収プロセスの進行は懸念の原因だった。 この取引を直接知るJSRの現・元幹部、政府関係者、投資家、銀行家、プライベート・エクイティ会社、業界ライバルへのインタビューでは、この物語が2022年11月のJSRのJICへの申し入れから始まったものではないことが示されている。

Months earlier Merck, a German healthcare and life sciences group, had proposed buying a majority stake in the Japanese company, according to two people with knowledge of its content. The approach vindicated those JSR executives who had feared it would be vulnerable to a bid after it completed the sale of its synthetic rubber business in April 2022. Merck declined to comment.

その内容に詳しい関係者2人によると、ドイツのヘルスケア・ライフサイエンスグループのメルクは数カ月前に日本企業の過半数株の購入を提案していたという。 このアプローチは、2022年4月に合成ゴム事業の売却を完了した後、入札に対して脆弱になるのではないかと懸念していたJSR幹部らの正しさを証明した。メルクはコメントを拒否した。

Its overture was immediately followed by similar approaches from at least two global buyout funds. One of them presented ideas that included carving out JSR’s remaining non-core businesses and taking the company private.

この提案の直後、少なくとも 2 つの世界的な買収ファンドから同様のアプローチがとられた。 そのうちの1社は、JSRの残りの非中核事業を切り出し、会社を非公開化することを含むアイデアを提示した。

By October, JSR’s board had considered and rejected Merck’s proposal, arguing that there was insufficient synergy. JSR said it received no offers for the business ahead of the JIC agreement, but added it received “a variety of transaction and collaboration ideas” on a regular basis.

10月までにJSR取締役会はメルク社の提案を検討し、相乗効果が不十分であるとして却下した。 JSRは、JIC契約前に事業のオファーはなかったと述べたが、定期的に「さまざまな取引や提携のアイデア」を受け取っていたと付け加えた。

JIC declined to comment on whether it was aware of the approach from Merck, saying it began deliberations after JSR proposed a deal on a “privately negotiated basis”.

JICはメルク社からのアプローチを認識していたかどうかについてはコメントを避け、JSRが「非公開交渉ベース」での取引を提案した後に検討を開始したと述べた。

There was also frustration within JSR’s boardroom over its financial performance; earnings per share were expected to fall to ¥40.95 this fiscal year, from ¥140.62 in the year ending March 2019, immediately before Johnson took over.

JSR の取締役会内では財務実績に対する不満もあった。 ジョンソン氏が就任する直前の2019年3月期の140.62円から今期は40.95円に低下すると予想されていた。

The market rise of JSR

JSRの市場上昇

Share price, ¥

株価、円

1 Eric Johnson named CEO

1 エリック・ジョンソンが CEO に就任

2 Announces sale of elastomers business to Eneos (completed in April 2022)

2 エネオスへのエラストマー事業譲渡を発表(2022年4月完了)

3 Merck submits proposal to JSR

3 メルクがJSRに提案書を提出

4 JSR announces takeover by JIC

4 JSR、JICによる買収を発表

5 JIC delays tender offer for JSR shares amid China antitrust probe

5 中国の独占禁止法捜査を受け、JICがJSR株の公開買い付けを延期

But the board held back from changing the management while talks with JIC were under way, although Nobuo Kawahashi stepped down as president last June. JIC has since said it plans to retain Johnson as chief executive, while ValueAct supported the JIC bid in light of the 35 per cent premium to the previous day’s closing price that it offered.

しかし、川橋信夫氏が昨年6月に社長を辞任したにもかかわらず、取締役会はJICとの協議が行われている間、経営陣の交代を控えた。 その後、JICはジョンソン氏を最高経営責任者として留任させる計画を発表したが、バリューアクトは、提示した前日終値に対する35%のプレミアムを考慮してJIC入札を支持した。

Several people involved with the process play down the idea that JIC’s involvement presages a new era of interventionism.

このプロセスに関与した何人かの関係者は、JIC の関与が介入主義の新たな時代を予感させるという考えを軽視している。

Andrew McDermott, founder of Japan-focused investment firm Mission Value Partners, says he does not think the JSR transaction and a similar one involving Toshiba represent a negative signal for broader merger and acquisition activity “because in these examples, you can see that Japan has an overarching strategic interest”.

日本に特化した投資会社ミッション・バリュー・パートナーズの創設者であるアンドリュー・マクダーモット氏は、JSR取引と東芝に関する同様の事件は、「これらの例では、日本が包括的な戦略的利益を持っていることがわかるため」、広範な合併・買収活動にとって否定的なシグナルとなっている。

Saito, at IwaiCosmo Securities, says that “it would be even more damaging to Japan’s reputation if the government let a company like JSR, which makes materials that are crucial to the production of next-generation semiconductor equipment, fall into foreign hands.”

「政府がJSR(それは次世代の半導体装置の製造にとって重要である材料を作ります)のような会社を外国の手に落ちさせるならば、それは日本の評判にさらに悪い影響を与えるでしょう」と、斎藤は、岩井証券で、言います。

But for long-term investors, the involvement of JIC made the Japanese government look suddenly more interventionist and seemed to contradict the notion that corporate Japan was becoming more responsive to shareholder pressure.

しかし長期投資家にとって、JICの関与は日本政府が突然介入主義的に見え、日本企業が株主の圧力により敏感になりつつあるという考えと矛盾しているように思えた。

Such investors have long known that many Japanese companies trade well below the book value of their assets, and have large cash piles and non-core assets they could sell. Companies have become more susceptible to pressure from shareholder activists; Hiromi Yamaji, the president of the group that controls the Tokyo Stock Exchange, has spoken out about the need to boost valuations and improve capital efficiency, giving activists a sense that they are now welcome.

そうした投資家は、多くの日本企業が自社資産の簿価を大幅に下回って取引されており、多額の現預金と売却できる非中核資産を抱えていることを以前から知っていた。 企業は株主活動家からの圧力に一層敏感になっている。 東京証券取引所を管理するグループの山路博美社長は、評価額の引き上げと資本効率の向上の必要性について発言しており、アクティビストらは今や歓迎されているとの感触を与えている。

Just a few weeks before its investment arm announced it was acquiring JSR, Meti published the first revisions to its guidelines on public takeovers in almost two decades. Companies are now expected to take any bona fide offer seriously and should establish a special committee to examine and report back on the attractiveness of that and any other bid.

投資部門がJSRの買収を発表するわずか数週間前に、Metiは株式公開買収に関するガイドラインの約20年ぶりの改訂版を発表した。 企業は現在、いかなる誠実な提案も真剣に受け止め、その入札やその他の入札の魅力を調査し、報告する特別委員会を設置することが求められている。

The guidelines were designed, say Meti officials, to stop Japanese chief executives arbitrarily rejecting unsolicited offers or accepting obviously inferior offers because they are from friendly or connected bidders. The changes bring Japanese companies into line with standard practice in the US and Europe, requiring them to seek out the highest price possible.

経産省当局者らによると、このガイドラインは、友好的な入札者やつながりのある入札者からのものであるという理由で、日本の最高経営責任者が一方的な申し出を恣意的に拒否したり、明らかに劣った申し出を受け入れたりするのを阻止するために策定されたという。 この変更により、日本企業は米国や欧州の標準的な慣行に沿ったものとなり、可能な限り最高の価格を追求することが求められている。

These and other reforms have made Japan’s substantial equity market a magnet for the world’s largest activist funds, including Elliott Management, Third Point, ValueAct and Effissimo.

こうした改革やその他の改革により、日本の実質的な株式市場は、エリオット・マネジメント、サード・ポイント、バリューアクト、エフィッシモなどの世界最大のアクティビスト・ファンドを引き寄せる磁石となった。

“The presence of ValueAct on the JSR shareholder register was among the main reasons we invested in it ourselves,” says the Tokyo-based portfolio manager of a major US fund. “The company had a non-core business we hoped they would sell, and a chips-related business we really liked.” He adds that recent history suggested the presence of an activist investor “creates a good chance of unlocking value quickly”.

「JSR株主名簿にValueActの存在があったことが、私たちが自らそれに投資した主な理由の一つでした」と、東京を拠点とする米国の大手ファンドのポートフォリオマネージャーは語る。 「その会社には、私たちが売却してほしいと考えていた非中核事業と、私たちが非常に気に入っていたチップ関連事業がありました。」 同氏は、最近の歴史を見ると、アクティビスト投資家の存在が「価値を迅速に解き放つ良いチャンスを生み出す」ことが示唆されていると付け加えた。

Some of this optimism melted away when JIC’s acquisition of JSR was announced, say shareholders. They questioned Johnson’s consolidation argument, with many considering it unlikely that JIC had been the only entity able or willing to buy the company.

株主らによると、JICによるJSR買収が発表されると、こうした楽観的な見方の一部は消え去ったという。 彼らはジョンソン氏の統合主張に疑問を呈しており、JICが同社を買収する能力がある、あるいは買収する意思がある唯一の企業である可能性は低いと多くの人が考えていた。

Even before the FT revealed that Merck had approached JSR, and before several private equity groups had also registered their interest in acquiring it, investors were suspicious. Had there been an effort to flush out other buyers and had all available offers been properly examined?

メルクがJSRに接近したことをFTが明らかにする前、またいくつかのプライベート・エクイティ・グループも買収に関心を示す前から、投資家は疑念を抱いていた。 他の購入者を追い出す努力があったのか、利用可能なオファーはすべて適切に検討されたのか?

In its statement disclosing the JIC offer, JSR said “indirect market checks” were in place in “an environment where other potential acquirers can make counterproposals”.

JICの提案を明らかにした声明の中で、JSRは「他の潜在的な買収者が対案を出せる環境」において「間接的な市場チェック」が実施されていると述べた。

Tadayuki Seki, a non-executive director at JSR who headed the special committee to review the JIC deal, says the process observed Meti’s M&A guidelines. “The board is entirely supportive” of the partnership with JIC and the JSR management, he adds.

JIC取引を検討する特別委員会の委員長を務めたJSRの非常勤取締役、関忠之氏は、このプロセスは経産省のM&Aガイドラインに従っていたと述べた。 JICおよびJSR経営陣とのパートナーシップを「取締役会は全面的に支持している」と同氏は付け加えた。

Seiji Takahashi, JSR’s chair, says the company has a “robust governance process and an active and engaged board that reviews all matters of material impact.” Other offers would have received the same scrutiny, he adds, but “none have been received.”

JSRの会長である高橋誠治氏は、同社には「強固なガバナンスプロセスと、重要な影響を与えるすべての問題を検討する活発で熱心な取締役会」があると述べた。 他のオファーも同様の精査を受けるはずだったが、「何も受け取られていない」と同氏は付け加えた。

But one London-based investor, who had always regarded JSR as an ideal target for Merck, other strategic buyers and private equity groups, says that any acquirer going up against the JIC bid would in effect be challenging the Japanese government: “You got to be realistic about the situation,” the investor adds. “They can’t buy it because the Japanese government have now said they cannot.”

しかし、ロンドンを拠点とするある投資家は、JSRをメルクや他の戦略的バイヤー、プライベート・エクイティ・グループにとって理想的なターゲットと見なしていたものの、JICの入札に対抗する買収者は、実質的に日本政府に挑戦することになると言う: 「状況について現実的に考えるべきです」と投資家は付け加える。「日本政府が買えないと言っているのだから、彼らは買えない」。

“JSR had been tripping up a lot on execution, especially on the life science side,” he adds. “So everything else being equal, it’s a frustrating outcome.”

「JSRは、特にライフサイエンス側で、実行時に多くのつまずきを抱えていました」と彼は付け加えた。 「他のすべてが同じだったとしても、悔しい結果だ。」

While investors try to work out what really happened, JSR’s own ambitions to drive consolidation in the semiconductor materials industry could be stymied by its sluggish financial performance.

投資家は何が起こったのか解明しようと努めているが、半導体材料業界の再編を推進するというJSR自身の野心は、業績の低迷によって妨げられる可能性がある。

The group suffered an operating loss of ¥2.75bn ($18mn) in the six months to September due to its struggling life science business. Following a cut to revenue and profit forecasts in November, Hidemitsu Umebayashi, an analyst at Daiwa, said JSR needed “to take measures to improve its own earnings” if it wants to achieve its “vision” for consolidation.

同グループはライフサイエンス事業の苦戦により、9月までの半年で27億5000万円(1800万ドル)の営業損失を被った。 11月に売上高と利益の予想を下方修正したことを受け、大和証券のアナリスト梅林秀光氏は、JSRが統合に向けた「ビジョン」を達成したいのであれば「自らの収益を改善するための措置を講じる」必要があると述べた。

Amid a weaker yen, and given their high market shares in certain technologies, bankers say Japanese companies will increasingly become targets for acquisition. But uncertainty over when and how the government may intervene could dampen such appetite, they warn. “Eric [Johnson] wouldn’t have wanted to be seen as selling off the crown jewels,” says one banker in Tokyo.

円安が進む中、特定の技術における高い市場シェアを考慮すると、日本企業はますます買収のターゲットになるだろうと銀行関係者らは言う。 しかし、政府がいつどのように介入するか不確実性があれば、そのような意欲が減退する可能性があると彼らは警告している。 「エリック(ジョンソン氏)は、王冠を売り飛ばしていると思われたくなかったでしょう」と東京のある銀行家は言う。

“But you have to wonder if what happened will make anyone else pause before making a bid.”

「しかし、今回の出来事で他の人が入札する前に立ち止まってしまうのではないかと考えなければなりません。」

英語学習と世界のニュースを!

自分が関心があることを多くの人にもシェアすることで、より広く世の中を動きを知っていただきたいと思い、執筆しております。もし、よろしければ、サポートお願いします!サポートしていただいたものは、より記事の質を上げるために使わせていただきますm(__)m