SASBスタンダードを学ぼう④ 真の「国際基準」への進化を目指して

本日のnoteは、昨日の内容の続きです。SASBがそのローカル性?を改善しグローバルに使用できる産業別開示基準にしていこうとするプロジェクト「International Applicability of the SASB Standards」について調べます。

なぜこのプロジェクトが実施されているのか

「International Applicability of the SASB Standards」に関する「About」のページを見るとわかります。(それにしてもこのページ、わかりやすい構造になっていますね…)

Following the consolidation of the Value Reporting Foundation (VRF) with the IFRS Foundation, the ISSB is responsible for the maintenance and enhancement of the SASB Standards. A small subset of the SASB Standards incorporate references to jurisdiction-specific laws and regulations which may be globally inapplicable, introduce regional bias, increase application costs and decrease the comparability and decision-usefulness of the resulting disclosures.

Timely enhancements to the international applicability of the SASB Standards are important to ensure these standards are suitable to be applied internationally—specifically to enable companies to develop disclosures regarding sustainability-related risks and opportunities in the absence of a specific IFRS Sustainability Disclosure Standard.

前段で、SASB基準の一部には「グローバルに適用できない固有の法律や規制(jurisdiction-specific laws and regulations which may be globally inapplicable)」などの内容が含まれている、と明記されています。

一方、後段を読むと「特に、IFRSのサステナビリティ開示基準がない場合(in the absence of a specific IFRS Sustainability Disclosure Standard)」にはSASBをの活用が期待されると書いてあります。SASBはIFRS発効後も重要であり続けたい、ということなのですね。

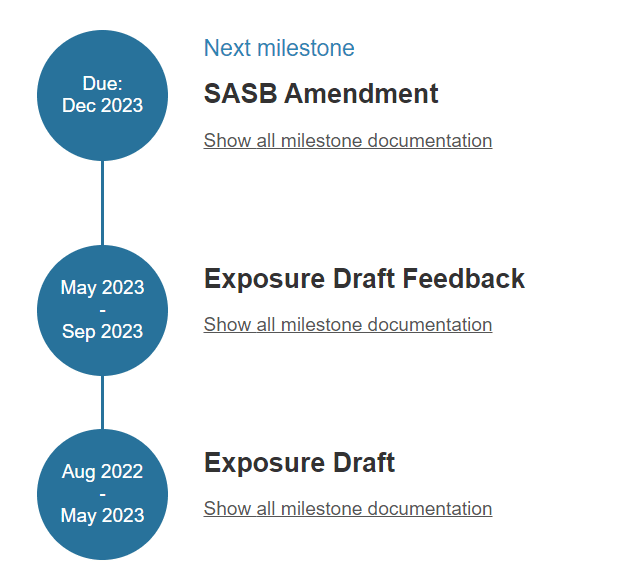

プロジェクトのスケジュールは?

「PROJECT HISTORY」のページに以下のような図が載っていました。

2023年12月(って今月ですね!)にSASBの修正版が提示される予定、ということでしょうか。楽しみです。

現在の状況は?

「CURRENT STAGE」のページによれば、10月11日、SASB基準の改訂を詳述した「ブラックライン文書(blackline documents)」が公表されているそうです。

このブラックライン文書には、ISSB公開草案「SASB®スタンダードの国際的な適用可能性を向上させるための方法論及びSASBスタンダード・タクソノミのアップデート」に対して寄せられたフィードバックが反映されているのだとか。

ということは、これが12月発表予定の最終案のベースになるということなのでしょうか…

のちほどこの「ブラックライン文書」も少し読んでみたいと思います。

以上、サステナビリティ分野のnote更新1000日連続への挑戦・56日目(Day56) でした。それではまた明日。

この記事が気に入ったらサポートをしてみませんか?