逆効果だったinternal devaluation

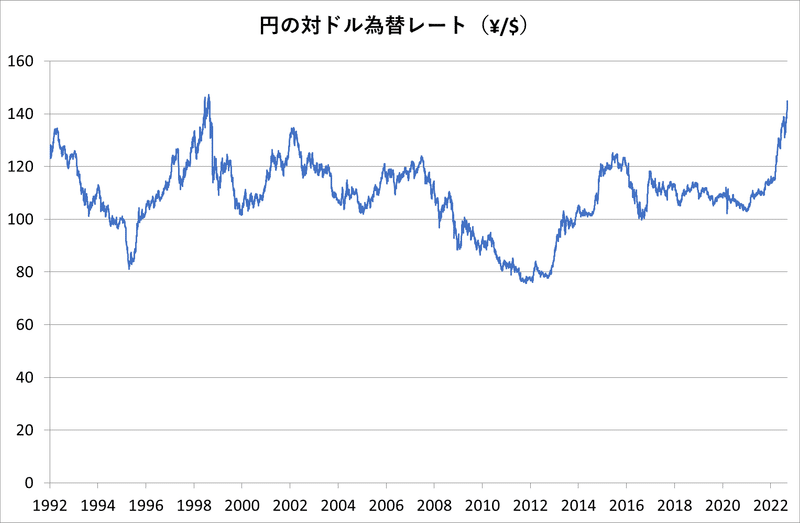

「ドル円はいよいよ1998年8月に付けた147円66銭が視野に入ってきた」が、

コラム:98年高値視野のドル円、為替介入の可能性はあるか=尾河眞樹氏 https://t.co/TjsiJgQxGB

— ロイター (@ReutersJapan) September 16, 2022

実質レートでは1998年8月を大きく下回り、変動相場制移行後の最低水準に達している。

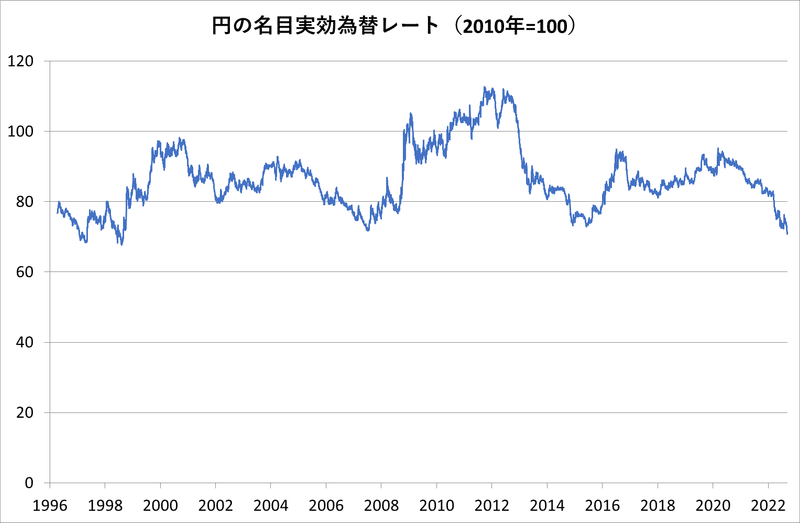

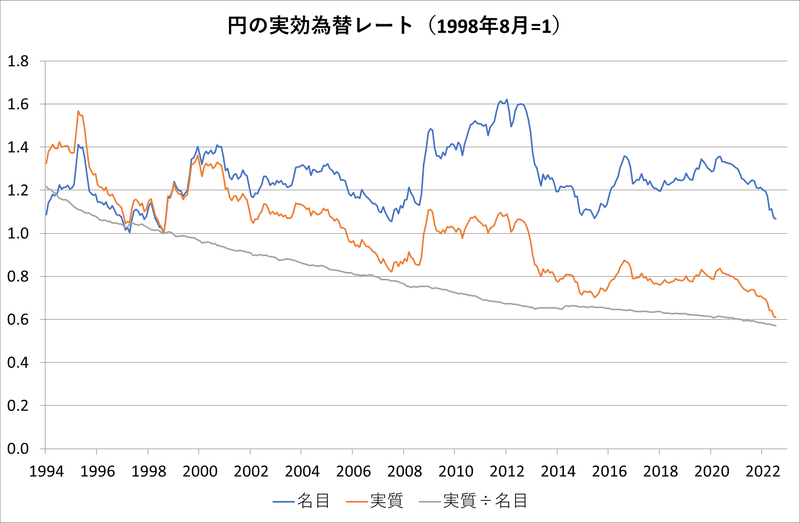

長期的に見ると、円の実質為替レートの減価はexternalよりもinternalのdevaluationの寄与が大きい。2022年7月を1998年8月とを比較すると、名目実効為替レートはわずかに円高だが、実質実効為替レートは4割も円安である。

ちなみに、プラザ合意前と比べても日本の実質実効為替レートは3割以上水準を下げてますが、名目実効レートとインフレ率格差に分解すると、名目実効レートはプラザ合意時と比べてむしろ77%以上円高水準になっており、相対的な物価水準が6割以上下がってます。

つまり、実質実効レートで見た日本の長期的な国際的購買力の低下は、円安ではなく低インフレ(デフレ)が主因です。

こうした視点からすれば、現時点で日本が金融引き締めに転じることは理にかなっていないといえるでしょう。

For countries that belong to—and want to stay in—a currency union, however, devaluation is not an option. This was the situation facing several euro area economies at the onset of the global financial crisis: capital had been flowing into these countries before the crisis but much of it fled when the crisis hit.

A remedy for these economies that has generated a lot of debate is so-called internal devaluation. This is a boost to competitiveness not through an (external) devaluation of the currency but by internal means, such as wage cuts or wage moderation.

日本は変動相場制にもかかわらず、external devaluation(円安)ではなくinternal devaluation(賃金抑制)の減価を続けてきたわけだが、それがworkしたとは言えない(というより有害だった)ことは明白だろう。

この記事が気に入ったらサポートをしてみませんか?