クルーグマンは又貸し説?

クルーグマンが現行の通貨制度の仕組みを理解していないことがわかるコラムを書いていた(本題は通貨発行益だが、それについてはさておく)。

— Paul Krugman (@paulkrugman) January 11, 2022

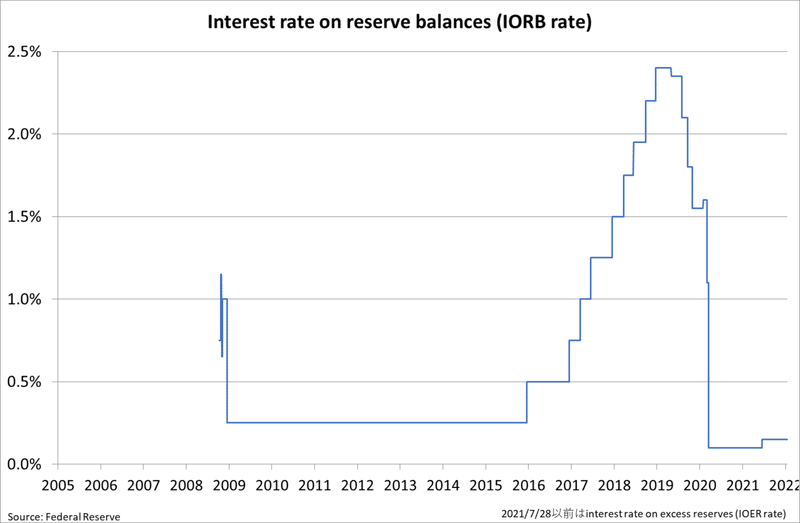

Since the 2008 financial crisis, however, banks have been voluntarily holding vast excess reserves, apparently because they don’t see enough good lending opportunities — and the Fed has been paying interest on these reserves, which makes them more like government debt than money the private sector was forced to accept.

2008年9月のリーマンショック以降、銀行は優良な貸出先が減ったために準備預金の超過準備を自発的に積み上げたという説明をしているが、準備預金の総額はFed(中央銀行)が決めるもので、個々の銀行の意向で決まるものではない。この説明からは銀行は中央銀行から供給された準備預金を民間企業や個人に又貸ししていると読み取れるが、そうではないことは日本の大学入試共通テストの出題にもあったとおりである。

本題から外れるがこれ👇も重要で、政府・中央銀行がインフレを制御できなくなると、財政支出に必要な通貨量も多くなり、その通貨供給が更なる物価上昇を招くという悪循環に陥ることがある。

High inflation, however, turns money into a hot potato people want to get rid of as quickly as possible, so the velocity of money — the rate at which it turns over — shoots up, which drives prices up even more. The problem is that as the value of money declines, the government has to print even more — in fact, has to increase the money supply at an even faster rate — in order to cover its deficits. This leads to even faster inflation, which leads to further rises in velocity, and the whole thing spirals into chaos.

高インフレによって政府も民間も支出の名目額は増えていくので、このグラフ👇の右上に位置することになるが、それが「積極財政による高度経済成長」を意味しないことは明らかである。

>(日経)財政出動の伸び率と経済の成長率に強い相関関係があるから、財政出動を増やせば経済が成長する、という暴論まである。@atkindmhttps://t.co/XPOYTrZV5H

— シェイブテイル (@shavetail) January 7, 2022

いえいえ。現実を無視しているのはアトキンソンさん。あなたですよ。そんな国は地球にはないんですから。 pic.twitter.com/5BJADM8nJo

狂乱物価にすれば実質経済成長率も高くなるのならどの国も苦労しない。

この記事が気に入ったらサポートをしてみませんか?