アセットマネージャーのためのファイナンス機械学習:ポートフォリオの構築 練習問題 CLA

minVarPort関数を、上限と下限の制約付きの最適化ができるCLAに置き換えて、NCO有りと無しでモンテカルトシミュレーションを行う。

上記のCLA.pyは細かなバグがあるので、修正した最終版が以下のコードになる。

#!/usr/bin/env python

#

# I (Martin Dengler) have been given the OK to upload this code to

# github, as long as I indicate:

#

# 1. That David H. Bailey and Marcos Lopez de Prado are the original

# authors.

#

# 2. That this code is provided under a GPL license for

# non-commercial purposes.

#

# 3. That the original authors retain the rights as it relates to

# commercial applications.

#

# The accompanying paper was published in an open-access application:

# http://ssrn.com/abstract=2197616

#

# The original code is here:

#

# http://www.quantresearch.info/CLA.py.txt

# http://www.quantresearch.info/CLA_Main.py.txt

#

# A sample dataset can be found here:

# http://www.quantresearch.info/CLA_Data.csv.txt

#

#

# On 20130210, v0.2

# Critical Line Algorithm

# by MLdP <lopezdeprado@lbl.gov>

#

# From: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2197616

#

# "All code in this paper is provided 'as is', and contributed to the

# academic community for non-business purposes only, under a GNU-GPL

# license"

#

import numpy as np

#---------------------------------------------------------------

#---------------------------------------------------------------

class CLA:

def __init__(self,mean,covar,lB=None,uB=None):

# Initialize the class

self.mean=mean

self.covar=covar

if(lB is None):

self.lB=np.full_like(mean,-1.)

else: self.lB=lB

if(uB is None):

self.uB=np.ones_like(mean)

else: self.uB=uB

self.w=[] # solution

self.l=[] # lambdas

self.g=[] # gammas

self.f=[] # free weights

#---------------------------------------------------------------

def solve(self):

# Compute the turning points,free sets and weights

f,w=self.initAlgo()

self.w.append(np.copy(w)) # store solution

self.l.append(None)

self.g.append(None)

self.f.append(f[:])

while True:

#1) case a): Bound one free weight

l_in=None

if len(f)>1:

covarF,covarFB,meanF,wB=self.getMatrices(f)

covarF_inv=np.linalg.inv(covarF)

j=0

for i in f:

l,bi=self.computeLambda(covarF_inv,covarFB,meanF,wB,j,[self.lB[i],self.uB[i]])

if l_in==None :l_in,i_in,bi_in=l,i,bi

elif l>l_in:l_in,i_in,bi_in=l,i,bi

j+=1

#2) case b): Free one bounded weight

l_out=None

if len(f)<self.mean.shape[0]:

b=self.getB(f)

for i in b:

covarF,covarFB,meanF,wB=self.getMatrices(f+[i])

covarF_inv=np.linalg.inv(covarF)

l,bi=self.computeLambda(covarF_inv,covarFB,meanF,wB,meanF.shape[0]-1,self.w[-1][i])

if (self.l[-1]==None or l<self.l[-1]):

if(l_out==None): l_out,i_out = l,i

elif l>l_out: l_out,i_out=l,i

if (l_in==None or l_in<0) and (l_out==None or l_out<0):

#3) compute minimum variance solution

self.l.append(0)

covarF,covarFB,meanF,wB=self.getMatrices(f)

meanF=np.zeros(meanF.shape)

else:

#4) decide lambda

if (l_in is not None):

if (l_out==None) or (l_in > l_out):

self.l.append(l_in)

f.remove(i_in)

covarF,covarFB,meanF,wB=self.getMatrices(f)

w[i_in]=bi_in # set value at the correct boundary

b=self.getB(f)

wB[b.index(i_in)]=bi_in

else:

self.l.append(l_out)

f.append(i_out)

covarF,covarFB,meanF,wB=self.getMatrices(f)

else:

self.l.append(l_out)

f.append(i_out)

covarF,covarFB,meanF,wB=self.getMatrices(f)

covarF_inv=np.linalg.inv(covarF)

#5) compute solution vector

wF,g=self.computeW(covarF_inv,covarFB,meanF,wB)

for i in range(len(f)):w[f[i]]=wF[i]

self.w.append(np.copy(w)) # store solution

self.g.append(g)

self.f.append(f[:])

if self.l[-1]==0:break

#6) Purge turning points

self.purgeNumErr(10e-10)

self.purgeExcess()

#---------------------------------------------------------------

def initAlgo(self):

# Initialize the algo

#1) Form structured array

a=np.zeros((self.mean.shape[0]),dtype=[('id',int),('mu',float)])

b=[self.mean[i][0] for i in range(self.mean.shape[0])] # dump array into list

a[:]=list(zip(range(self.mean.shape[0]),b)) # fill structured array

#2) Sort structured array

b=np.sort(a,order='mu')

#3) First free weight

i,w=b.shape[0],np.copy(self.lB)

while sum(w)<1:

i-=1

w[b[i][0]]=self.uB[b[i][0]]

w[b[i][0]]+=1-sum(w)

return [b[i][0]],w

#---------------------------------------------------------------

def computeBi(self,c,bi):

if c>0:

bi=bi[1][0]

if c<0:

bi=bi[0][0]

return bi

#---------------------------------------------------------------

def computeW(self,covarF_inv,covarFB,meanF,wB):

#1) compute gamma

onesF=np.ones(meanF.shape)

g1=np.dot(np.dot(onesF.T,covarF_inv),meanF)

g2=np.dot(np.dot(onesF.T,covarF_inv),onesF)

if wB is None:

g,w1=float(-self.l[-1]*g1/g2+1/g2),0

else:

onesB=np.ones(wB.shape)

g3=np.dot(onesB.T,wB)

g4=np.dot(covarF_inv,covarFB)

w1=np.dot(g4,wB)

g4=np.dot(onesF.T,w1)

g=float(-self.l[-1]*g1/g2+(1-g3+g4)/g2)

#2) compute weights

w2=np.dot(covarF_inv,onesF)

w3=np.dot(covarF_inv,meanF)

return -w1+g*w2+self.l[-1]*w3,g

#---------------------------------------------------------------

def computeLambda(self,covarF_inv,covarFB,meanF,wB,i,bi):

#1) C

onesF=np.ones(meanF.shape)

c1=np.dot(np.dot(onesF.T,covarF_inv),onesF)

c2=np.dot(covarF_inv,meanF)

c3=np.dot(np.dot(onesF.T,covarF_inv),meanF)

c4=np.dot(covarF_inv,onesF)

c=-c1*c2[i]+c3*c4[i]

if c==0:return

#2) bi

if type(bi)==list:bi=self.computeBi(c,bi)

#3) Lambda

if wB is None:

# All free assets

return float((c4[i]-c1*bi)/c),bi

else:

onesB=np.ones(wB.shape)

l1=np.dot(onesB.T,wB)

l2=np.dot(covarF_inv,covarFB)

l3=np.dot(l2,wB)

l2=np.dot(onesF.T,l3)

return float(((1-l1+l2)*c4[i]-c1*(bi+l3[i]))/c),bi

#---------------------------------------------------------------

def getMatrices(self,f):

# Slice covarF,covarFB,covarB,meanF,meanB,wF,wB

covarF=self.reduceMatrix(self.covar,f,f)

meanF=self.reduceMatrix(self.mean,f,[0])

b=self.getB(f)

covarFB=self.reduceMatrix(self.covar,f,b)

wB=self.reduceMatrix(self.w[-1],b,[0])

return covarF,covarFB,meanF,wB

#---------------------------------------------------------------

def getB(self,f):

return self.diffLists(range(self.mean.shape[0]),f)

#---------------------------------------------------------------

def diffLists(self,list1,list2):

return list(set(list1)-set(list2))

#---------------------------------------------------------------

def reduceMatrix(self,matrix,listX,listY):

# Reduce a matrix to the provided list of rows and columns

if len(listX)==0 or len(listY)==0:return

matrix_=matrix[:,listY[0]:listY[0]+1]

for i in listY[1:]:

a=matrix[:,i:i+1]

matrix_=np.append(matrix_,a,1)

matrix__=matrix_[listX[0]:listX[0]+1,:]

for i in listX[1:]:

a=matrix_[i:i+1,:]

matrix__=np.append(matrix__,a,0)

return matrix__

#---------------------------------------------------------------

def purgeNumErr(self,tol):

# Purge violations of inequality constraints (associated with ill-conditioned covar matrix)

i=0

while True:

if i==len(self.w):break

w=self.w[i]

for j in range(w.shape[0]):

if w[j]-self.lB[j]<-tol or w[j]-self.uB[j]>tol:

del self.w[i]

del self.l[i]

del self.g[i]

del self.f[i]

break

i+=1

#---------------------------------------------------------------NCOからこのCLAを呼ぶコードは以下の通りになる。上限は全ての資産で$${+1.}$$、下限を$${-1.}$$とし、空売りを許した。

import numpy as np

import pandas as pd

import MarPat as MP

import ONC as NC

def CLA_nco(cov, mu, lB=None, uB=None, maxNumClusters=None,minVarPortf=True):

import CLA

cov = pd.DataFrame(cov)

mu = pd.Series(mu[:,0])

corr1 = MP.cov2corr(cov)

corr1, clstrs, _ = NC.clusterKMeansBase(corr1, maxNumClusters, n_init=10)

wIntra= pd.DataFrame(0, index=cov.index, columns=clstrs.keys(),dtype='float64')

lB_=None

uB_=None

for i in clstrs:

cov_ = cov.loc[clstrs[i], clstrs[i]].values

mu_ = mu.loc[clstrs[i]].values.reshape(-1,1)

if(lB is not None): lB_ = lB.loc[clstrs[i]].values.reshape(-1,1)

if(uB is not None): uB_ = uB.loc[clstrs[i]].values.reshape(-1,1)

cla=CLA.CLA(mu_,cov_,lB_,uB_)

cla.solve()

if(minVarPortf==True):

wIntra.loc[clstrs[i], i] = cla.w[-1].flatten()

else :

max_sr, max_w_sr = cla.getMaxSR()

wIntra.loc[clstrs[i], i] = max_w_sr.flatten()

cov_= wIntra.T.dot(np.dot(cov, wIntra))

mu_ = wIntra.T.dot(mu)

mu_ = mu_.values.reshape(-1,1)

if(lB is not None):

lB_ = wIntra.T.dot(lB)

lB_ = lB_.values.reshape(-1,1)

if(uB is not None):

uB_ = wIntra.T.dot(uB)

uB_ = uB_.values.reshape(-1,1)

cla=CLA.CLA(mu_,cov_.values,lB_,uB_)

cla.solve()

if(minVarPortf==True):

wInter= pd.Series(cla.w[-1].flatten(), index=cov_.index)

else:

max_sr, max_w_sr = cla.getMaxSR()

wInter= pd.Series(max_w_sr.flatten(), index=cov_.index)

nco = wIntra.mul(wInter, axis=1).sum(axis=1).values.reshape(-1,1)

return nco

def CLAExp(mu0,cov0,lB=None, uB=None,

nObs=1000, nSims=1000 , minVarPortf = True,shrink=False):

w1 = pd.DataFrame(0, index=range(0, nSims),

columns=range(0, cov0.shape[0]),dtype='float64')

w1_d = pd.DataFrame(0, index=range(0, nSims),

columns=range(0, cov0.shape[0]),dtype='float64')

for i in range(0, nSims):

mu1, cov1 = MP.simCovMu(mu0, cov0, nObs, shrink=shrink)

cla=CLA.CLA(mu1,cov1,lB,uB)

cla.solve()

if(minVarPortf == True):

w1.loc[i] = cla.w[-1].flatten()

else:

max_sr, max_w_sr = cla.getMaxSR()

w1.loc[i] = max_w_sr.flatten()

w1_d.loc[i] = CLA_nco(cov1, mu1, lB, uB,int(cov1.shape[0]/2),minVarPortf).flatten()

return w1, w1_d

def main():

nBlocks, bSize, bCorr = 10, 5, .5

q=10.0

np.random.seed(0)

mu0, cov0 = MP.formTrueMatrix(nBlocks, bSize, bCorr)

minVarPortf=True

w1, w1_d=CLAExp(mu0=mu0,cov0=cov0,minVarPortf = minVarPortf)

cla=CLA.CLA(mu0,cov0.values)

cla.solve()

w0 = cla.w[-1]

w0 = np.repeat(w0.T, w1.shape[0], axis=0)

print('minVar Markowitz RMSE: ',

round(np.mean((w1-w0).values.flatten()**2)**.5,4))

print('minVar NCO RMSE:',

round(np.mean((w1_d-w0).values.flatten()**2)**.5,4))

minVarPortf=False

w1, w1_d=CLAExp(mu0=mu0,cov0=cov0,minVarPortf = minVarPortf)

max_sr, w0 = cla.getMaxSR()

w0 = np.repeat(w0.T, w1.shape[0], axis=0)

print('maxSR Markowitz RMSE: ',

round(np.mean((w1-w0).values.flatten()**2)**.5,4))

print('maxSR NCO RMSE:',

round(np.mean((w1_d-w0).values.flatten()**2)**.5,4))

if __name__ == '__main__':

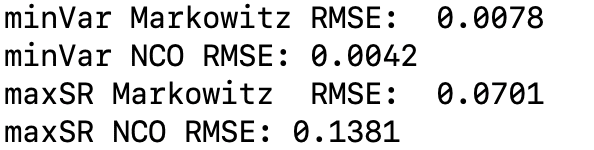

main()このコードの結果は以下のようになった。

この記事が気に入ったらサポートをしてみませんか?